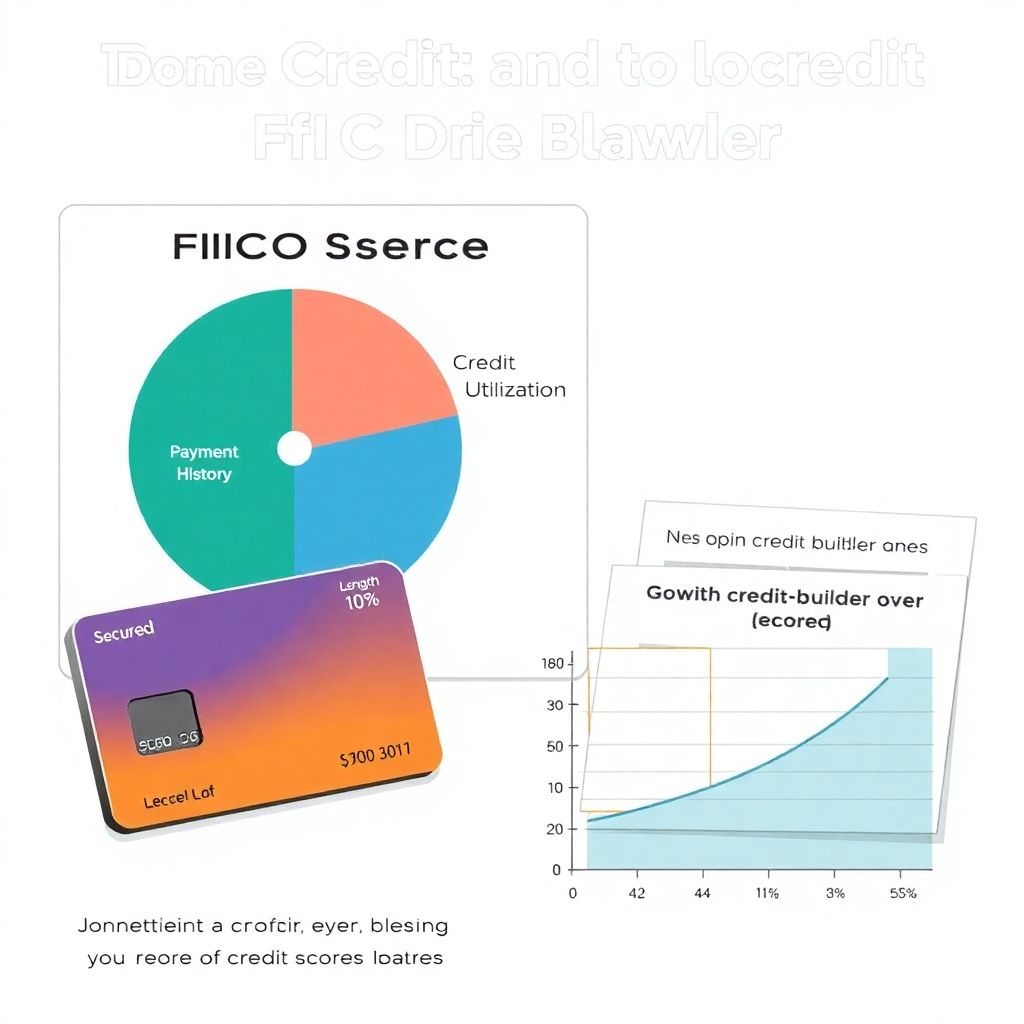

Understanding Credit: Definitions and Core Concepts

Credit refers to a contractual agreement in which a borrower receives something of value now and agrees to repay the lender at a later date, typically with interest. A credit score, typically ranging from 300 to 850, is a numerical representation of a person’s creditworthiness, calculated based on their credit history. The three major credit bureaus in the United States—Equifax, Experian, and TransUnion—collect and maintain consumer credit information. The FICO Score, developed by the Fair Isaac Corporation, is the most widely used credit scoring model. It evaluates five key categories: payment history (35%), credit utilization (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

A diagrammatic representation of the FICO model would resemble a pie chart with the above percentages, where the largest segments are payment history and credit utilization. These factors are critical for individuals starting from zero credit, as they directly impact the speed and quality of credit score development.

Starting from Zero: Establishing a Credit File

For individuals without any credit history—commonly referred to as “credit invisibles”—the first step is to create a credit file. According to the Consumer Financial Protection Bureau (CFPB), as of 2023, approximately 19% of U.S. adults were either credit invisible or had unscored credit records. This represents a slight decline from 21% in 2021, indicating a growing awareness and proactive behavior among young adults and immigrants.

The most accessible tools for initiating a credit profile include secured credit cards, credit-builder loans, and becoming an authorized user on someone else’s existing credit account. A secured credit card requires a refundable security deposit, typically equal to the card’s credit limit. For example, a $300 deposit grants a $300 credit limit. The cardholder then uses the card for small purchases and repays the balance on time to build a positive payment history.

Credit-builder loans function differently. Financial institutions hold the borrowed amount in a locked account while the borrower makes fixed monthly payments. Upon completion, the funds are released, and a record of on-time payments is reported to credit bureaus. These loans are particularly effective for individuals with no prior credit, as they simulate real loan behavior without the risk of defaulting on a large sum.

Strategic Use of Credit: Utilization and Payment Behavior

Once a credit account is active, maintaining low credit utilization is essential. Credit utilization ratio is calculated by dividing the total revolving credit used by the total available credit. For instance, if a user has a $1,000 credit limit and uses $300, the utilization is 30%. FICO recommends keeping this ratio below 30% to avoid score penalties.

Payment history remains the most influential factor in credit scoring. Missing even one payment can significantly impact a new credit score. According to Experian’s 2024 data, individuals with no missed payments in their first 12 months of credit usage were 63% more likely to reach a score above 700 within two years, compared to just 28% among those with one or more delinquencies.

To visualize this, imagine a line graph showing credit score progression over 24 months. The line representing users with perfect payment records rises steadily, while the line for those with delinquencies rises more slowly or fluctuates downward after missed payments.

Comparison with Alternative Credit Models

Traditional credit scoring models rely heavily on historical data from conventional credit products. However, alternative data models have emerged to address the limitations faced by credit newcomers. These models incorporate rental payments, utility bills, and subscription services into credit evaluations. For instance, Experian Boost allows users to link their bank accounts and include utility and telecom payments in their credit files.

While these models can accelerate initial credit development, they are not universally accepted by all lenders. A comparative analysis shows that while traditional FICO scores are used in over 90% of lending decisions, alternative data models are primarily used by fintech lenders and subprime credit issuers. Therefore, while beneficial, these alternatives should complement—not replace—traditional credit-building methods.

Monitoring Progress and Avoiding Pitfalls

Once credit is established, continuous monitoring is vital. Free credit monitoring services from platforms like Credit Karma or Experian provide real-time alerts about score changes, new account openings, and potential fraud. Reviewing credit reports annually from AnnualCreditReport.com ensures accuracy and helps identify errors. According to the Federal Trade Commission (FTC), 21% of consumers in 2022 found at least one error on their credit reports that could affect their scores.

Common pitfalls for rookies include over-applying for credit, which triggers multiple hard inquiries and can temporarily lower scores. Additionally, closing old accounts can reduce the average age of credit, negatively impacting the score. Instead, maintaining long-standing accounts, even with minimal activity, contributes positively to the length of credit history metric.

Conclusion: Long-Term Credit Strategy for Rookies

Building credit from scratch is a structured process that requires strategic planning, consistent behavior, and financial discipline. By starting with secured credit products, maintaining low utilization, and making timely payments, individuals can establish a robust credit profile within 12 to 24 months. Supplementing traditional methods with alternative data sources can further enhance credit visibility, especially for underserved populations.

As of 2025, the average FICO score in the United States stands at 718, up from 714 in 2023, reflecting a national trend toward improved credit behavior. For credit rookies, aligning with this trend involves not only initiating credit activity but also cultivating sustainable financial habits that support long-term credit health.