Why Taxes Matter So Much in Your 30s

If you’re in your 30s in 2025, you’re investing in a totally different world than your parents did. Back in the 1980s and 1990s, most people relied on company pensions, picked a few mutual funds, and barely thought about tax optimization. Today pensions are almost gone, markets are more global, and every extra percent you lose to taxes and fees really hurts the long‑term compounding of your money. That’s why the best tax efficient investments in your 30s are not just about chasing returns, but about structuring your accounts so that the government doesn’t quietly skim off more than it has to over the next 30–40 years. Your 30s are prime time: you usually earn more than in your 20s, but still have a long runway for growth, which makes tax planning feel less like a “bonus” and more like a core investing skill.

Short History: How We Got to Today’s Tax-Smart Investing

To understand today’s tax-smart strategies, it helps to see the arc of the last few decades. In the 1970s and 1980s, tax advantaged retirement accounts for 30 year olds were basically just 401(k)-type plans and traditional IRAs, often with clunky paper statements and high-fee mutual funds. The Roth IRA only arrived in the late 1990s, and early on many people ignored it because they expected to be in a lower tax bracket later. Then two things changed: fees dropped dramatically with index funds and ETFs, and online brokerages made it insanely easy to trade. In the 2010s and early 2020s, robo‑advisors, tax‑loss harvesting algorithms and phone apps made sophisticated tax moves accessible to regular investors. By 2025, we live in a world where you can open an account, project your lifetime tax bill, and automate a tax strategy in under an hour—something that would have looked like sci‑fi to investors in 1990.

Key Tax-Smart Buckets: Accounts First, Investments Second

A common mistake in your 30s is to obsess over which stock or ETF to pick, and barely think about what kind of account you’re using. From a tax perspective, the “wrapper” often matters more than the specific investment. If you want to know how to reduce taxes on investments in your 30s, the first move is to rank your accounts: 1) tax‑advantaged retirement accounts (401(k), Roth IRA, etc.), 2) health‑related tax shelters like HSAs where available, and only then 3) regular taxable brokerage accounts. Historically, people put everything in one place and hoped for the best; now the smarter approach is to match asset types with the right tax shelter. For example, bond funds and REITs that throw off a lot of taxable income fit better inside retirement accounts, while broad stock index funds, which are already relatively tax‑efficient, can sit in a taxable account without as much damage.

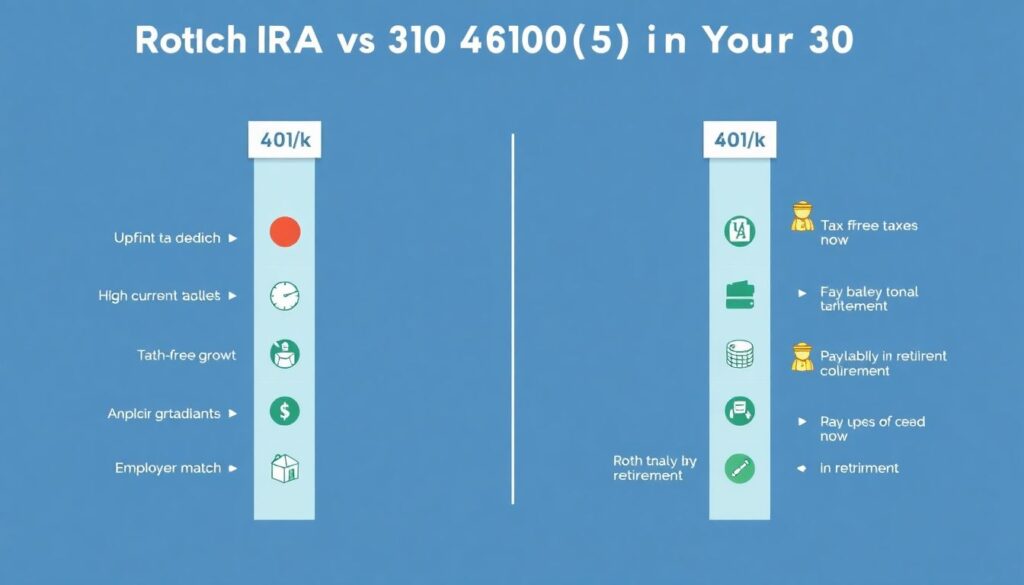

Roth IRA vs 401(k): Which Is Better in Your 30s?

The classic question—roth ira vs 401k which is better in your 30s—doesn’t have a one‑size‑fits‑all answer, but there are some useful rules of thumb. A traditional 401(k) usually gives you an upfront tax deduction, which is great if you’re in a high tax bracket today. A Roth IRA, on the other hand, gives up the deduction now in exchange for tax‑free withdrawals later, including on all the growth. For many people in their 30s whose income is rising but not yet at peak, a blended strategy often works best: contribute at least enough to the 401(k) to grab the employer match (that’s free money), then add to a Roth IRA for tax diversification, and only then circle back to max the 401(k) if you can. Historically, workers leaned almost exclusively on pre‑tax 401(k) contributions. The shift in the 2010s and 2020s toward Roth options—even Roth 401(k)s—reflects a growing awareness that tax rates in retirement might not be as low as everyone once assumed.

Comparing Different Tax-Smart Approaches

When people talk about the best tax efficient investments in your 30s, they usually mean one of three broad approaches. First, there is the “max your tax shelters” strategy: stuff as much as possible into retirement accounts and let compounding do its thing. Second, there is the “optimize everything” approach, where you think about asset location, tax‑loss harvesting, and even which ETFs have the lowest distributions. Third, there is the “delegate” path: you pay for tax planning services for investors in their 30s or use a sophisticated robo‑advisor to handle all the moving parts. All three can work; the main difference is how hands‑on you want to be. Historically, only wealthy families bothered with complex tax strategies through private banks. Now even smaller investors can imitate many of those moves with low‑cost technology and a bit of education, which levels the playing field.

Tech Tools: Pros and Cons of Modern Tax Optimization

Technology has completely changed how to reduce taxes on investments in your 30s, but it’s not magic. Robo‑advisors and brokerage platforms in 2025 can automatically scan your portfolio for losses, harvest them, and replace sold funds with similar ones to avoid wash‑sale issues. The upside is obvious: automation saves time, increases discipline, and applies tax rules consistently. The downside is that algorithms don’t know your full life plan unless you feed them accurate info, so they might harvest losses you’d prefer to keep for long‑term conviction holdings. There’s also the risk that people become passive passengers, never really understanding what’s happening in their account. The middle ground is powerful: use tech to handle repetitive tasks (like tax‑loss harvesting, dividend reinvestment, and rebalancing) while still making the big-picture choices—how much risk to take, which accounts to prioritize, and when to tap a human expert.

Human Pros vs Algorithms: Choosing the Right Help

Professional tax planning services for investors in their 30s have also evolved. In the past, you either did it alone or hired an expensive advisor. Now, you can pick from a spectrum: low-cost robo‑advisors, hybrid services that combine software with occasional human calls, or full‑service planners who coordinate investing and tax filing. The main advantages of human help are nuance and context: a person can factor in things like career changes, stock options, plans to move countries, or taking time off for kids. The perks of technology are cost and speed; many automated platforms cost less than a typical advisory fee and still implement good, research‑backed strategies. The trick is matching the complexity of your life to the level of help you pay for. If you have stock options, side‑business income, or cross‑border issues, a human with tax expertise usually beats a chatbot inside your brokerage app.

Practical Recommendations: Building a Tax-Smart Game Plan

To turn all this into action, it helps to map out a simple step‑by‑step structure. Think of it as a checklist you refine over time rather than a rigid rulebook. Your situation will change—salary jumps, possible career breaks, buying a home, kids—and your tax strategy should flex with that. But in your 30s, certain priorities tend to repeat across many people’s lives, which means you can lean on a basic order of operations before adding fancy optimization tricks or speculative bets that blow up your tax return.

1. Capture any employer retirement match first.

2. Build an emergency fund so you’re not raiding investments.

3. Add to Roth accounts if you expect income to climb.

4. Then consider maxing pre‑tax contributions if your bracket is high.

5. Only after that, invest in a taxable account with tax‑efficient funds.

Each step tightens the leak in your “tax bucket” so that more of your return actually stays in your name instead of disappearing every April.

Comparing Investments: What’s Actually Tax-Efficient?

Once accounts are sorted, you can look at what usually qualifies as the best tax efficient investments in your 30s from an asset-type perspective. Broad stock index ETFs are typically very tax‑friendly in taxable accounts because they trade less and distribute fewer capital gains; historically, this has made them a favorite for long‑term taxable portfolios. Actively managed mutual funds, by contrast, often churn their holdings more, kicking off short‑term gains that get taxed at higher rates. Real estate can be tax‑smart through depreciation and certain deductions, but rental income is still taxable and the paperwork can be intense. In tax‑advantaged retirement accounts, you have more freedom to hold income-heavy assets like bond funds or REITs, because the dividends and interest are sheltered until withdrawal (or forever, in the Roth case). The big comparison is not “Is this fund good?” but “Is this fund in the right type of account for its tax behavior?”

Pros and Cons of Modern Investing Technologies

It’s easy to get dazzled by apps that promise to optimize everything for you, so it’s worth spelling out the real pros and cons. On the plus side, modern platforms can minimize taxes by automatically placing assets in the most efficient accounts, timing trades to stay in long‑term capital gains territory, and using detailed tax reports that plug straight into your filing software. On the downside, no tool can change the basic tax laws; if you trade constantly, chase hot ideas, or ignore contribution limits, technology can only clean up so much. There’s also the privacy angle: your detailed financial data is now stored on servers, sometimes analyzed for product recommendations. In 2025, the trend is toward more transparent algorithms and better user control over data, but you still need to read the fine print and accept that some trade‑off between convenience and privacy is part of modern investing.

2025 Trends: What’s New in Tax-Smart Investing for 30‑Somethings

Several fresh trends in 2025 are shaping how to reduce taxes on investments in your 30s. First, more employers now offer Roth options inside workplace plans, which lets you solve the roth ira vs 401k which is better in your 30s question partly inside a single account by splitting contributions between pre‑tax and Roth buckets. Second, ESG and climate-focused funds are no longer fringe, and many now use the same tax‑efficient ETF structures as traditional index funds, making it easier to combine values-based investing with tax efficiency. Third, governments in several countries have tightened rules around day trading and derivatives, so the historical “YOLO trading” trend from the late 2010s now carries more tax friction and reporting complexity. The big picture trend is that tax‑smart investing is no longer a niche skill—it’s becoming table stakes for anyone serious about building wealth over multiple decades.

How to Choose Your Own Tax-Smart Strategy in Your 30s

Picking a path comes down to honesty about your habits, time and tolerance for complexity. If you prefer simplicity, focusing on basic tax advantaged retirement accounts for 30 year olds, broad index funds, and a simple contribution plan already puts you far ahead of the average investor. If you enjoy the details, layering in tax‑loss harvesting, careful asset location, and periodic check‑ins with a professional can squeeze extra value out of your portfolio. You might decide to use low‑cost software for routine optimizations and then pay for hour‑based tax planning services for investors in their 30s every year or two, just to sanity‑check big decisions like buying a home, exercising stock options, or switching countries. The key is consistency: tax laws may shift, markets will definitely shift, but a habit of checking the tax impact of every major investment move is what will keep more of your returns compounding for your future, not slipping away unnoticed.

Комментарии

У них на сайте есть подробности по этапам работ и можно сразу записаться на консультацию с руководителем: строительству домов в Сочи. Для тех, кто не из региона и строит удалённо, это прям спасение — всё под контролем и по адекватным ценам.