Why money skills became a survival skill, not a “nice‑to‑have”

Over the last three years the money landscape for young people has turned from “confusing” to “borderline hostile”. In 2023, US credit‑card balances passed $1.08 trillion (New York Fed), and buy‑now‑pay‑later use among Gen Z jumped sharply according to multiple industry reports. At the same time, TikTok and YouTube are full of crypto “gurus” and options traders. Without basic financial literacy, teens and young adults walk into this environment unarmed, making expensive mistakes long before they earn a stable income.

Что именно входит в финансовую грамотность для подростков

When we talk about financial literacy for teens, we mean a specific toolkit: understanding income and taxes, building a simple budget, knowing how interest works, and using credit without wrecking a score before 21. Good financial education programs for high school students also touch on student loans, workplace benefits, and the basics of investing. It’s less about turning every 17‑year‑old into an analyst and more about preventing avoidable damage in the first five to seven years of adult life.

Реальные истории: как одно решение стоит тысяч долларов

Consider a very typical case from 2022–2024: an 18‑year‑old gets a first credit card “for emergencies”, then starts using it for gas and food. Without a budget, balances creep up; with a 24% APR, a $1,500 balance and only minimum payments can cost over $900 in interest and take years to clear. I’ve seen similar patterns with store cards and BNPL plans: four or five small “no‑interest” purchases overlap, and suddenly there’s a cash‑flow crisis that forces late fees, overdrafts and more borrowing.

Технический блок: как работает сложный процент на долги

“`text

Example: $1,500 credit card, 24% APR, minimum payment 3% (or $35).

• Month 1 interest ≈ $30 (1,500 × 0.24 ÷ 12)

• If you only pay the minimum, most of that first payment is interest.

• Total payoff time: ~7–8 years

• Total interest paid: $800–1,000+

Key takeaway: “I’ll pay it off later” gets very expensive when the rate is above 20%.

“`

Почему именно последние три года усилили риск для молодежи

From 2022 to 2024, prices rose faster than wages for many entry‑level jobs, especially in housing and food. That pushed more young adults to rely on credit just to keep up. At the same time, brokerage apps removed trading commissions, and crypto platforms aggressively targeted Gen Z. Surveys in 2023 showed a growing share of 18‑ to 24‑year‑olds owning volatile assets but lacking even a basic emergency fund. This combination of high living costs and easy speculation magnifies the cost of not learning money skills early.

Статистика: что говорят цифры о подростках и деньгах

Across OECD countries, recent PISA assessments show that about one in four 15‑year‑olds struggles with basic financial tasks, like comparing simple loan offers. In the US, various 2022–2024 surveys consistently find that fewer than 20–25% of teens can correctly answer three core money questions on interest, inflation and risk. At the same time, teen spending power remains huge: American teenagers control or influence tens of billions of dollars annually, much of it spent digitally where impulsive decisions are easiest.

Почему школа и дом не успевают за реальностью

Most parents were never systematically taught about money themselves, so advice at home tends to be fragmentary or outdated. Meanwhile, only a portion of states and countries mandate standalone financial education programs for high school students, and where they exist, they’re often squeezed into a few hours. The result is a gap: teens learn calculus before they learn how student‑loan interest is calculated, or how a late payment can haunt their credit reports for seven years and raise the cost of every future loan.

Роль структурированных курсов и онлайн‑обучения

This is where structured financial literacy courses for teens make a real difference. Unlike casual social‑media advice, good courses build concepts in order: earning, spending, saving, then credit and investing. For university‑age learners balancing part‑time work and study, online money management classes for young adults add flexibility; they can walk through real paystubs, bank statements and loan offers, pausing to test understanding. When those courses use current examples—BNPL, gig‑work income, digital wallets—engagement and retention improve sharply.

Практический блок: базовый каркас личных финансов

“`text

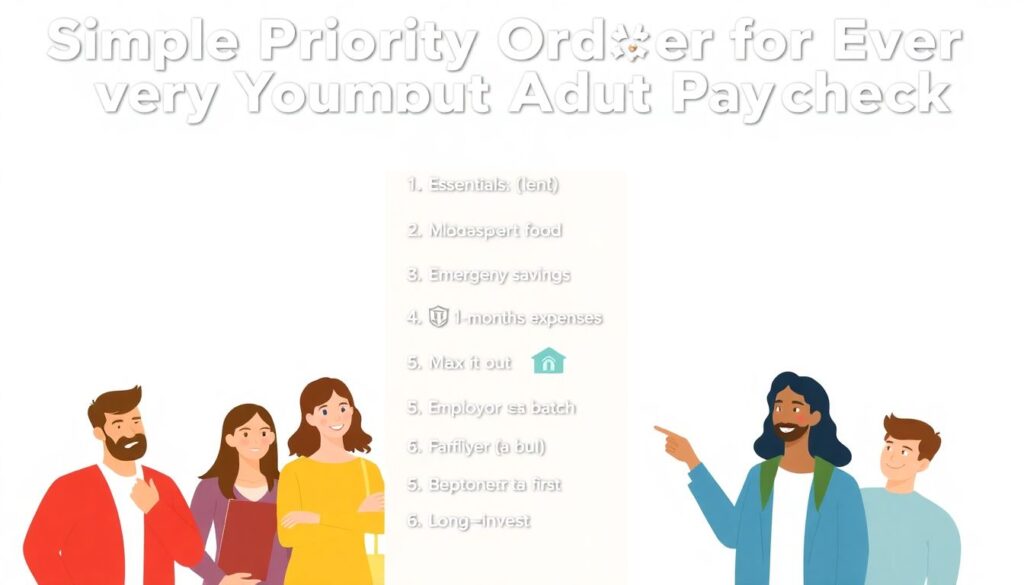

Simple priority order for every young adult paycheck:

1. Essentials: rent/transport/food

2. Minimum debt payments (never skip)

3. Emergency savings: target 1–3 months expenses

4. Employer match (if offered): max it out

5. Extra debt repayment (focus highest rate first)

6. Long-term investing (broad, low-cost funds)

This framework is simple enough for a teen yet robust enough to scale with income.

“`

Бюджетирование: как цифры превращают стресс в контроль

Budgeting gets a bad reputation as restrictive, but for teenagers it usually feels more like permission to spend intentionally. The most effective financial literacy courses for teens give hands‑on practice: tracking one month of real expenses, then categorizing and adjusting. Over the past three years, app‑based budgeting tools have made this far easier; teens don’t need spreadsheets, just a clear view of where money actually goes. Once they see leak points—food delivery, in‑game purchases—small tweaks free up savings without feeling like deprivation.

Инструменты: какие приложения реально помогают подросткам

When talking about the best budgeting apps for teenagers, three criteria matter more than brand names: simplicity, automation and parental controls. Apps that sync with bank accounts, round up purchases into savings and send spending alerts help teens link actions to outcomes. Some platforms allow shared views so parents can coach without micromanaging. The details differ, but the principle is constant: reduce friction in tracking, and budgeting becomes a five‑minute weekly check‑in instead of a dreaded monthly chore that never happens.

Инвестиции: почему ранний старт бьет даже высокий доход

Compound growth is where starting young creates a structural advantage. A 19‑year‑old who invests $150 a month at a 7% annual return until 29 and then stops entirely can end up with a similar retirement balance as someone who starts at 30 and invests the same amount until 65. This is why investment courses for young adults beginners emphasize time horizon over stock‑picking. The skill is not “beating the market”, it’s learning to automate contributions, avoid emotional trading, and keep costs and taxes low.

Технический блок: формула сложного роста для инвестиций

“`text

Future Value = Payment × [((1 + r)^n – 1) ÷ r]

Example:

• Monthly investment: $150

• Annual return (r): 7% = 0.07

• Years (n): 10

Future Value ≈ $150 × 138 ≈ $20,700

You contributed $18,000 and earned about $2,700 in growth.

Stretch this over 40+ years and compounding dominates contributions.

“`

Кредитный рейтинг: невидимый балл, который решает вашу аренду

Credit scores may feel abstract to a 19‑year‑old, right up until an apartment application gets denied or a car loan quote comes back with a painful interest rate. Over the last three years, more landlords, employers and insurers have leaned on credit data. Late payments, collections or defaulted phone contracts now follow young adults into housing and job markets. Teaching teens to use one low‑limit card, pay in full, and avoid co‑signing for friends is a cheap way to buy future flexibility.

Цифровые ловушки: как соцсети и игры монетизируют импульсы

Modern money traps are often embedded in interfaces teens use daily: loot boxes in games, creator tipping, and one‑click subscriptions that are easy to start and hard to cancel. Algorithms are designed to nudge frequent small purchases, which don’t feel like “spending money” but quietly drain accounts. From 2022 to 2024, regulators in several countries have raised concerns about these models, yet the burden still falls on users. Financial literacy helps young people recognize these mechanics and build small frictions back in.

Как выстроить обучение: от теории к действию

To move from knowing to doing, programs must integrate practice. Strong financial education programs for high school students weave in projects: planning a mock move‑out budget, comparing phone plans, or analyzing real‑world loan offers. For college students or early‑career workers, online money management classes for young adults can require uploading anonymized screenshots of actual statements and building a plan based on them. The more the content touches real decisions—this month, this paycheck—the more likely habits are to stick.

Список навыков, которые стоит освоить до 20 лет

– Creating a simple monthly budget and updating it at least once

– Understanding how interest works on both savings and debt

– Reading a paystub: taxes, deductions, and net vs gross income

– Using one credit product responsibly and knowing your credit score

– Building an emergency buffer and starting long‑term investing early

Как родителям и школам действовать уже сейчас

For parents, the most effective step in 2025 is to bring teens into real money conversations: show the family budget, explain trade‑offs, and let them manage a small, regular sum with accountability rather than control. Schools can partner with nonprofits or fintechs to offer modular financial literacy courses for teens that fit into existing subjects like math or social studies. Neither setting has to be perfect; consistency and relevance matter more than a glossy one‑off “money day” that students forget by next week.

Итог: финансовая грамотность как форма личной свободы

When you look at the last three years—rising costs, record consumer debt, speculative manias—it’s clear that financial literacy is no longer a niche interest. For teens and young adults, it is a core life competency, as basic as digital literacy or written communication. The payoff is not just a bigger bank balance; it’s the ability to say no to predatory offers, yes to opportunities, and to change paths without being locked in by bad past decisions. In a volatile economy, that freedom might be the most valuable asset of all.