Why “Financially Responsible” Beats “Bigger Is Better”

Planning a financially responsible wedding isn’t about stripping away all the joy; it’s about refusing to start your married life under a pile of debt. In simple terms, a financially responsible wedding is an event where your total costs do not damage your long‑term financial health. That means you can pay all the invoices on time, still keep an emergency fund, and avoid high‑interest debt like credit cards or payday loans. Compared with the “traditional” approach of “we’ll figure it out later,” this method favors clarity, limits, and conscious trade‑offs instead of impulse decisions and social pressure.

If you compare it with a luxury, no‑limits celebration, the responsible version rarely looks worse; it just looks more intentional. You’re still buying meaning and memories, but you’re cutting the parts that mostly feed vendors’ margins and Instagram expectations. Think of it as choosing a tailored suit that fits you perfectly instead of renting an oversized designer label just because others expect it. The goal is simple: a day you’re proud of that still lets you sleep well when the credit card bill arrives.

—

Step 1. Translate “Dream Wedding” Into Real Numbers

Before you do anything else, you need a concrete budget. In finance, a budget is a plan that assigns every expected unit of income to a category of expected expense, with limits you promise not to exceed. For weddings, that means you calculate how much money is available from you, your partner, and any family contributions, and you lock in a total ceiling. That top line number is not a vague wish; it’s a hard constraint, like a maximum safe load for a bridge. The difference between couples who stay on track and those who don’t is whether that number is negotiable every time they see a pretty centerpiece.

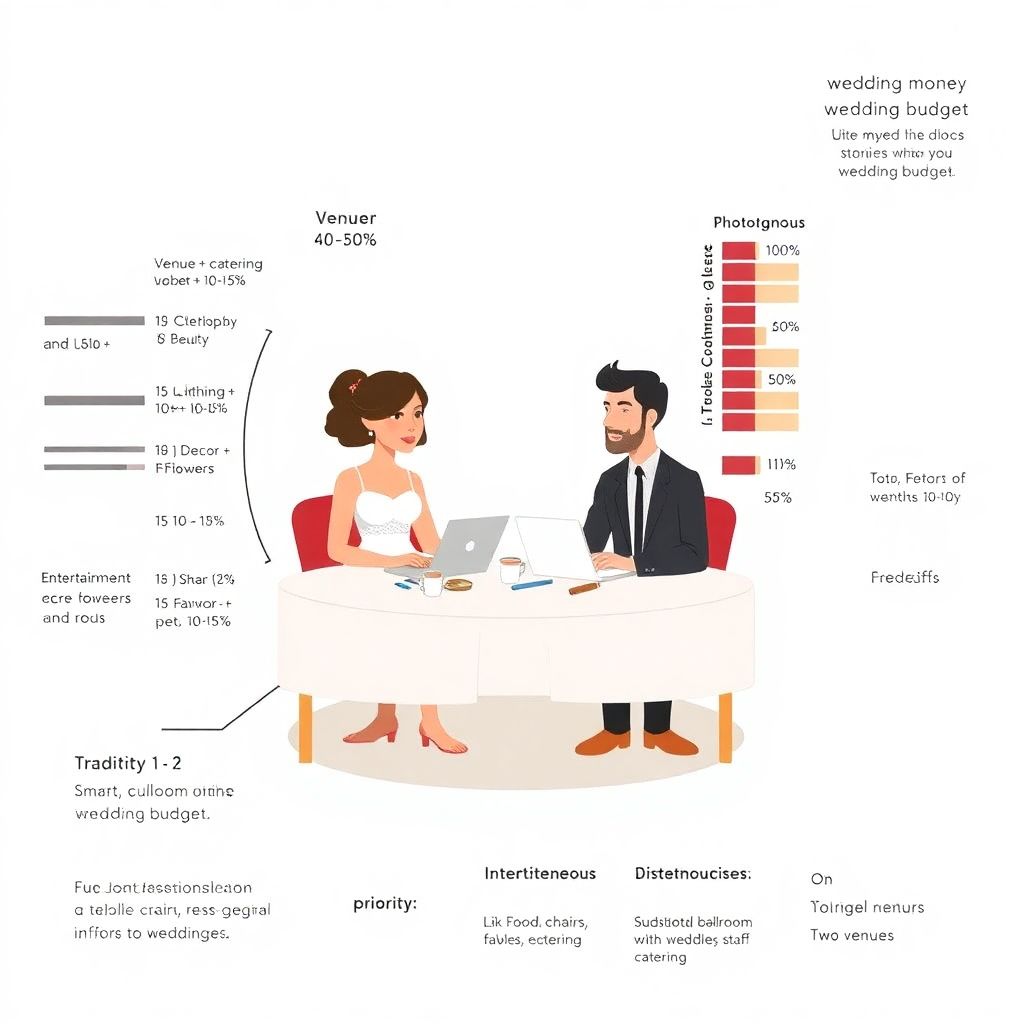

Here’s a simple text “diagram” to visualize a financial framework for the day. Imagine your total budget as a circle cut into slices. For a lean but comfortable wedding, a common distribution might look like this:

– Venue + catering: about 40–50% of the circle

– Photography + video: about 10–15%

– Clothing + beauty: about 10–15%

– Decor + flowers: about 5–10%

– Entertainment: about 5–10%

– Miscellaneous (stationery, transport, gifts, license, buffer): about 10–15%

You can picture each slice occupying part of the circle. When one slice expands, another must shrink. That’s the key mental model: every “yes” to an upgrade is a “no” to something else, not to mention a possible “no” to your future savings. When you hear people ask how to plan a wedding on a budget, what they’re really asking is how to control the size of each slice of that circle without hating the result.

—

Step 2. Define and Rank Your Priorities as a Couple

A financially responsible wedding assumes you can’t maximize everything at once. In decision‑making terms, you’re managing trade‑offs: when resources are limited, more of one thing means less of another. To keep resentment at bay, you and your partner need to rank what matters most, not what looks best online. That means turning “we want everything perfect” into a ranked list that shows where you’re willing to splurge and where you’ll happily cut corners. Compared with blindly copying a Pinterest board, this method gives you a personalized optimization problem, not a generic checklist.

A practical way to do it: each of you lists your top five priorities in order. Examples might include “amazing food,” “great photos,” “live band,” or “intimate guest list.” Then you merge your lists and agree on a final ranking. If you both put photography at the top, it deserves a bigger budget slice; if decor lands at the bottom, that’s your first candidate for savings. By making the trade‑offs explicit, you stop arguing about tiny details and start asking better questions like “does this expense lift one of our top priorities or just fill space?” Over time, that question becomes a habit that keeps your wallet intact.

—

Diagram: Priority vs. Spend Alignment

Picture a vertical list of priorities from 1 (most important) to 5 (least). Next to it, imagine bars that show how much you actually plan to spend on each category. For a financially responsible wedding, the tallest bars should line up with the highest priorities. If you notice a long bar next to a low‑priority item like favors or limo rental, that mismatch is a visible warning. You can “trim” that bar and reassign the funds to something that will actually matter in five years, like photography or a honeymoon fund. This kind of mental diagram helps you quickly see when emotion, not logic, is driving your spending.

—

Step 3. Understand and Speak the Right Money Language

To negotiate and compare offers, you need a few basic financial terms clear in your mind. Fixed costs are expenses that don’t change with the size of your wedding, such as a marriage license, officiant fee, or dress alterations. Variable costs change depending on your guest count or level of service, like catering per person, chair rentals, or bar packages. In practice, controlling variable costs—especially the number of guests—is one of the most powerful levers you have if you’re serious about a financially responsible wedding.

Another key concept is opportunity cost: the value of what you give up when you choose one option instead of another. For example, spending an extra $2,000 on a designer gown may mean postponing building an emergency fund or cutting a honeymoon in half. The gown’s real cost isn’t just the price tag; it’s all the experiences and security that money could have bought. When you think in these terms, you automatically start looking for budget friendly wedding ideas that keep opportunity costs low while still delivering emotional value. Instead of “can we afford it right now,” you start asking “is this the best use of this money compared with everything else we care about?”

—

Step 4. Choosing the Right Venue Without Losing Your Shirt

The venue is often the single largest component of your budget, which is why it deserves more analysis than “the photos look nice.” A venue contract usually includes rental time, included services (tables, chairs, linens), and sometimes catering and bar packages. Places that bundle food and beverage may look more expensive on paper but can simplify logistics and reduce hidden costs. In contrast, a “blank space” warehouse might be cheap to rent but more costly once you add rentals, decor, and outside catering. Comparing venues means looking at the total package cost, not just the headline rental fee.

When you catch yourself googling low cost wedding venues near me, remember that “low cost” doesn’t only mean a lower rental price. Seasonal and time‑of‑day choices matter a lot. A Friday evening or Sunday brunch wedding in the same location can be significantly cheaper than a Saturday night while giving you nearly identical photos and memories. Public spaces like parks, community halls, and small museums often cost a fraction of traditional ballrooms, especially if you’re open to off‑peak dates. The responsible approach is to list your top three realistic venue options, calculate the all‑in cost for each, and then ask which one aligns with your budget and priorities, not your ego.

—

Comparing Venue Types: Traditional vs. Alternative

A traditional hotel ballroom might include staff, tables, chairs, and catering, which reduces stress but often demands you choose their pre‑set menus and bar packages. On the other hand, a local community center or art studio gives you more control over vendors and decor but requires extra coordination. If you’re leaning heavily on cheap wedding planning services for support, an all‑inclusive venue can offset some of those planning costs. If you’re organized and comfortable managing multiple suppliers, an alternative venue can deliver the same emotional impact at a lower total price. The responsible choice comes down to your time, energy, and comfort with logistics, not just which room looks poshest.

—

Step 5. Vendors: DIY, Friends, or Pros?

Vendor selection is where a lot of couples overspend without realizing it, often because they feel obligated to follow an “industry standard.” To think more clearly, classify each task as must‑hire professional, safe to DIY, or potential friend/family collaboration. A must‑hire pro might be a licensed caterer (for food safety and logistics) or an experienced photographer (you don’t get a re‑do on photos). Safe DIY could be simple decor or playlists for parts of the day. Friend collaborations might work for officiating, dessert baking, or stationery design—but only if you have honest conversations and back‑up plans.

This is also where you’ll bump into offers from affordable wedding planners or partial coordination services. Compared with going fully solo, affordable wedding planners can actually save money if they use their experience and vendor network to avoid costly mistakes and negotiate better deals. At the same time, not every couple needs full‑service planning. If your budget is tight, consider day‑of coordination or consulting packages over luxury planning. It’s similar to hiring a tax professional: if your situation is complex, the fee often pays for itself; if it’s simple, you might lean more on your own research and targeted advice sessions.

—

When “Cheap” Planning Services Make Sense (and When They Don’t)

You’ll likely see ads for cheap wedding planning services, especially online. The key is to distinguish between “cheap because efficient” and “cheap because low value.” Efficient services might offer streamlined packages, digital tools, and standardized processes that reduce their costs without undermining your experience. Low‑value services, in contrast, might involve poor communication, limited expertise, or careless execution that ends up costing you more in corrections and stress. Use references, detailed contracts, and clear deliverables to figure out which camp a service belongs to. A planner who calmly protects your budget and negotiates on your behalf is a cost control asset, not a luxury.

—

Step 6. Guest List: The Most Powerful Lever You Have

From a technical perspective, guest count is your strongest cost multiplier. Every additional guest increases variable costs—food, drink, chairs, invitations, favors, sometimes transportation. If catering is $70 per person and you add 20 people, that’s $1,400 plus tax and service fees. Treat each new guest as a line item with a real financial impact, not an abstract headcount. Unlike fixed costs, this is a lever you can pull decisively: fewer people means more money per person for quality, or savings that can move directly into your future financial goals.

To keep things balanced, some couples build a “guest capacity” based on their venue and meal budget and then work backward. For example, if you can comfortably spend $10,000 on food and beverages and the per‑person rate is $80, your maximum realistic guest count is 125. If your current list is at 180, you know you must either trim the list or change the catering model (buffet vs. plated, brunch vs. dinner, limited bar vs. open bar). This kind of calculated approach might feel cold at first, but it actually protects you from emotional pressure down the line by giving you a rational boundary to point to.

—

Step 7. Smart Saving Moves That Feel Good, Not Cheap

Being financially responsible doesn’t mean your wedding needs to feel stripped‑down or joyless. The trick is to find budget friendly wedding ideas that save serious money without slashing your emotional return. That could mean opting for a cocktail reception with substantial appetizers instead of a full formal dinner, or mixing fresh greenery with fewer premium blooms to stretch your florals. Whenever you brainstorm a cost‑cutting move, ask two questions: “How much does this really save?” and “How much will we actually care about this in ten years?” Unimportant but expensive details are prime candidates for reduction.

Here are areas where many couples can trim spending without noticeable pain:

– Switching from printed RSVP cards to online RSVPs to cut stationery and postage.

– Choosing a DJ plus curated playlists instead of a large band, especially for smaller venues.

– Renting decor items instead of buying, or buying used from local resale groups.

Notice that none of these changes how married you’ll be at the end of the day. They simply redirect funds away from disposable extras and toward your savings, debt repayment, or honeymoon. Over time, that choice compounds: interest you don’t pay on credit cards becomes money you can invest or use for a home deposit. That’s the long shadow cast by your wedding decisions.

—

DIY vs. Professional: A Practical Comparison

DIY can be a powerful tool when you’re asking how to plan a wedding on a budget, but it’s not automatically cheaper. Your time, skills, and stress levels are all part of the cost. If you spend three weekends hand‑crafting intricate invitations, the “savings” might not be worth the exhaustion, especially if you end up buying extra materials to fix mistakes. Paying a professional for a clean, simple design could actually be more economical in both money and mental health. Before committing to DIY, list the materials, tools, time, and possible failure points. If any of those look big, consider a simpler project or a pro. Financially responsible isn’t just about dollars; it’s also about protecting your bandwidth.

—

Step 8. Building a Realistic Timeline and Cash Flow Plan

Another technical term that quietly matters is cash flow, which describes when money comes in and goes out. Many vendors require retainers or deposits months in advance and final payments shortly before the wedding. If you don’t map these payments against your expected income and savings, you may end up relying on high‑interest credit to bridge gaps even though your overall budget looked reasonable on paper. A financially responsible wedding treats time like a resource: you use a schedule to spread out both decisions and payments.

Create a month‑by‑month view from “today” to your wedding date and mark every known payment due date and amount. Then overlay your expected income and savings contributions. If a cluster of large payments appears in the same month, you can proactively adjust: negotiate slightly different payment schedules, cut or downgrade items, or increase your savings rate temporarily. A simple mental “bar chart” works here: imagine each month as a vertical bar representing money needed, and another bar showing money available. If any expense bar towers over your income bar, you need to rebalance. This approach protects you from last‑minute scrambles that lead to bad, expensive decisions.

—

Step 9. When and How to Use Professional Help Wisely

Not everyone needs full‑service planning, but almost everyone benefits from at least a bit of expert guidance. If your job is intense, your wedding is logistically complex, or you have family dynamics that add stress, a planner or coordinator can be a strategic investment. Instead of thinking of them as a “luxury add‑on,” treat them as a potential cost control mechanism. Some affordable wedding planners offer modular services: a few strategy sessions, vendor recommendations, and a day‑of coordination package. Compared with muddling through alone, this limited support can prevent expensive missteps such as non‑refundable deposits on poorly chosen vendors or last‑minute rush fees.

At the same time, you don’t want to outsource your entire financial responsibility. No planner knows your long‑term goals, debt situation, or risk tolerance better than you do. The healthiest dynamic is a partnership: you set the hard budget and priorities; they use their operational knowledge to execute that vision efficiently. If you ever feel nudged toward upgrades that don’t align with your stated financial limits, see that as a red flag. The right professional is someone who helps you protect your boundaries, not someone who encourages you to stretch “just a bit” every time you hesitate.

—

Step 10. Protecting Your Future Beyond the Wedding Day

A wedding is a single day; your marriage is (hopefully) decades. In financial planning terms, your wedding is a short‑term goal, while buying a home, building retirement savings, or starting a family are long‑term goals. A financially responsible approach keeps short‑term spending from undermining those long‑term objectives. One practical method is to set a ratio: decide that for every dollar you spend on the wedding, a certain amount also goes toward a shared savings target. Even a modest rule like “for every $4 we put into the wedding, we put $1 into our emergency fund” shifts your mindset toward balance.

By the time the wedding is over, you’ll remember the moments: the vows, the laughter, the people who showed up for you. You’re unlikely to remember whether the napkins matched the exact color of your bouquet. Framing your decisions through that lens makes it easier to say no to expenses that only exist to impress others or live up to someone else’s idea of “proper.” In the end, a financially responsible wedding is evidence that you and your partner can make thoughtful, values‑driven decisions together. That skill is more valuable than any centerpiece and will serve you far beyond your big day.

—

Practical Checklist to Keep You Grounded

To finish, here’s a concise checklist you can mentally run through as you plan:

– Have we set a clear total budget and agreed not to exceed it?

– Do our biggest expenses line up with our top shared priorities?

– Are we controlling variable costs like guest count and catering style?

– Have we compared venues and vendors on total cost, not surface price?

– Do our payment timelines match our income and savings capacity?

If you can honestly answer “yes” to those questions, you’re not just planning an event—you’re practicing the kind of financial teamwork that keeps couples stable and resilient. That, more than any display of extravagance, is what makes a wedding truly worth celebrating.