Why Freelancers Need to Treat Taxes Like a Business Problem

When you go freelance, nobody withholds taxes from your paycheck.

That feels great in the beginning… until your first big tax bill lands and you realize: “Wait, I owe how much?”

As a freelancer you’re effectively running a small business, even if it’s just you and a laptop at the kitchen table. That means new rules, new forms, and unfortunately—new ways to make expensive mistakes.

This guide walks you through the core of understanding your tax obligations as a freelancer, with real-life examples, specific numbers, and the most common beginner errors to avoid.

—

Employee vs. Freelancer: What Actually Changes

When you were an employee:

– Your employer withheld income tax automatically

– They also paid half of your Social Security and Medicare

– In many cases, you just filed a simple return once a year

As a freelancer (in the U.S. context):

– Nobody withholds taxes for you

– You pay both the employee and employer share of Social Security & Medicare (called self-employment tax)

– You usually need to pay estimated taxes quarterly, not once a year

The self-employment tax in real numbers

> Technical block: Self-employment tax basics (U.S.)

> – Self-employment tax rate: 15.3%

> – 12.4% for Social Security

> – 2.9% for Medicare

> – Applies to net profit from freelancing (income minus expenses)

> – Kicks in when your net self-employment income is $400 or more in a year

> – Paid on Schedule SE, attached to Form 1040

This self-employment tax is on top of federal (and usually state) income tax. That’s why many new freelancers feel blindsided.

—

The #1 Beginner Mistake: Forgetting Taxes Aren’t “Optional” Money

New freelancers often treat all incoming money as available spending money.

Example from practice

Alex, a new freelance designer, made $60,000 in her first year:

– She didn’t track expenses systematically

– She didn’t set aside money for taxes

– She assumed “I’ll sort it out at tax time”

At filing time, her approximate numbers looked like this (simplified):

– Income: $60,000

– Expenses (laptop, software, workspace, etc.): $10,000

– Net profit: $50,000

Rough tax impact (very rough illustration, federal only, single filer):

– Self-employment tax:

– $50,000 × 15.3% ≈ $7,650

– Federal income tax (after standard deduction, etc.): roughly another $3,000–$5,000

Total bill: well over $10,000 owed.

Alex had a few thousand in savings. The rest went on a credit card.

This shock is extremely common—and completely avoidable.

—

How Much to Set Aside for Taxes

There’s no perfect one-size-fits-all number, but for many U.S.-based freelancers:

– 25–30% of net income is a reasonable starting rule of thumb

– Higher-earning freelancers or those in high-tax states might need 30–35%

Better to slightly over-save and get a refund than to scramble for cash.

> Technical block: Simple tax reserve formula

> 1. Track your monthly freelance income (total deposits from clients).

> 2. Estimate expenses at, say, 20–30% of that if you’re still new and not tracking precisely.

> 3. From the remaining amount, move 25–30% into a separate “tax” savings account every month.

> 4. Do not use that account for anything else.

—

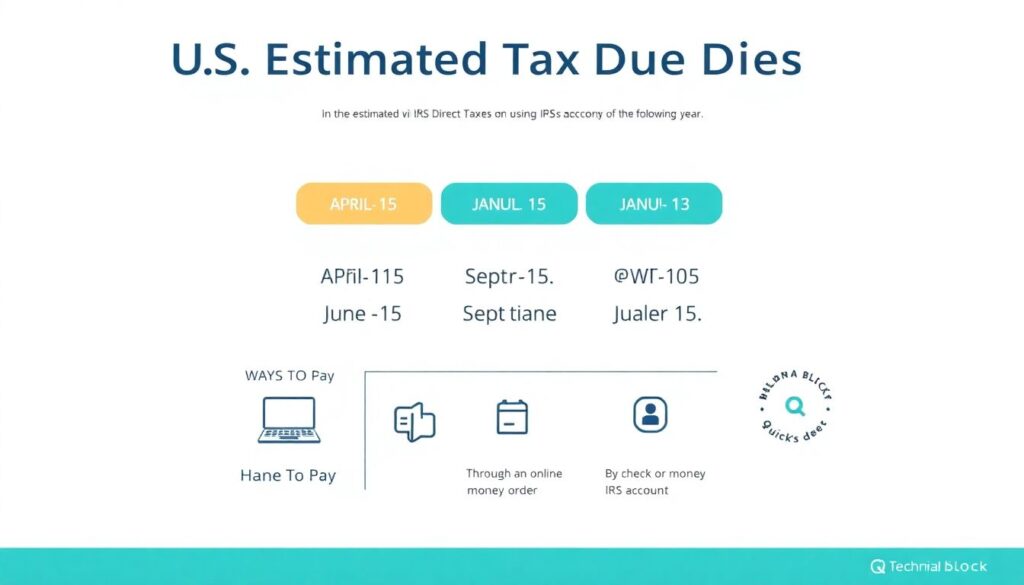

Quarterly Taxes: How to Pay Like a Pro

If you expect to owe at least $1,000 in tax for the year, the IRS wants you to make estimated quarterly payments.

That’s where many beginners trip up—they only think about taxes in April.

How to pay quarterly taxes as a freelancer

In the U.S., typical due dates for estimated taxes:

– April 15

– June 15

– September 15

– January 15 (of the following year)

You can pay:

– Online via IRS Direct Pay using a bank account

– Through an online IRS account

– By check or money order (less common nowadays)

> Technical block: Quick quarterly estimate method

> 1. Take your expected annual net profit from freelancing.

> 2. Multiply by your effective tax rate (say 25–30% as a rough estimate).

> 3. Divide the result by 4.

> 4. That’s your quarterly payment target. Adjust as your income changes.

If your income fluctuates wildly (very common in freelancing), you can recalculate mid-year. It’s better to adjust than stay locked into a bad estimate.

—

Common Tax Forms Freelancers Should Recognize

You don’t need to memorize form numbers, but you should know what they mean when they show up.

Most common:

– Form 1099-NEC – Issued by clients who paid you $600 or more during the year

– Schedule C – Where you report your freelance income and expenses

– Schedule SE – Calculates self-employment tax

– Form 1040 – Your main individual tax return

Missing a 1099 or forgetting to report income is a classic mistake—and yes, the IRS often knows, because they get copies too.

—

Freelance Deductions: What You Can Actually Write Off

Another beginner error: either not deducting enough (overpaying) or deducting everything under the sun (risking an audit).

Common, legit freelancer deductions (if they’re ordinary and necessary for your work):

– Laptop, monitor, and other gear

– Software subscriptions (Adobe, Notion, coding tools, etc.)

– Online services (website hosting, email services, cloud storage)

– Professional education, courses, conferences

– Part of your home expenses, if you qualify for the home office deduction

– Business-related travel and a portion of your phone/internet

> Technical block: Simple home office deduction (U.S.)

> – Simplified method: $5 per square foot, up to 300 sq ft

> – Max simplified deduction: $1,500 per year

> – Space must be used regularly and exclusively for business

Overstating deductions (“I’ll just write off my entire rent and car”) is a beginner mistake that can backfire quickly in an audit.

—

Real-World Mistakes New Freelancers Make

Let’s break down some of the most expensive beginner moves in practical terms.

1. Mixing personal and business money

You get paid into your personal account, pay for groceries, flights, software, and think “I’ll sort receipts later.”

Problems:

– Hard to prove which expenses are business vs personal

– Nightmare to reconstruct at tax time

– Easier to miss deductions or create suspicious patterns

Fix: Open a separate checking account just for freelance income and expenses. Even if you’re not an LLC yet, this is an immediate upgrade.

—

2. Ignoring small expenses (they add up)

Many beginners only track the “big stuff” (laptop, desk) and ignore:

– $12 monthly app subscriptions

– $15 domain renewals

– $49 online trainings

– $8 stock photo purchases

Over a year, these can easily total hundreds or thousands of dollars. At a 25% tax rate, missing $2,000 in deductions can mean $500 in extra tax you didn’t need to pay.

—

3. Waiting until April to deal with anything

Freelancers who only think about taxes once a year usually:

– Don’t pay quarterly

– Don’t keep proper records

– Panic in April and rush through filing

This is where freelancer tax filing services or a freelancer tax accountant near me search can actually save you money, not just time, because they’ll often spot missed deductions and planning opportunities.

—

4. Trusting only generic tools without understanding the basics

Using the best tax software for freelancers can be incredibly helpful, but software can only work with the information you feed it. If you:

– Misclassify expenses

– Forget income from certain clients

– Don’t understand self-employment tax

…even the best tool will give you the wrong result.

Tax software is a tool, not a substitute for basic understanding.

—

When It Makes Sense to Call in a Professional

For very simple situations, software might be enough:

– One or two clients

– Straightforward expenses

– No employees, no complicated state rules

But consider talking to a pro when:

– Your freelance income becomes your main income source

– You cross into higher tax brackets

– You have multiple income streams (courses, affiliate income, consulting, etc.)

– You’re thinking about forming an LLC or S-corp

Many people start with a search like “self-employed tax preparation services” or “freelancer tax accountant near me” and schedule at least a one-time consultation.

That single meeting can:

– Set up your bookkeeping system

– Clarify what you can and can’t deduct

– Help you estimate quarterly payments accurately

– Prevent years of repeated mistakes

—

Simple Systems to Stay Out of Trouble

You don’t need to become an accountant. You just need a few habits.

Try this lightweight system:

– One bank account for business income/expenses

– One savings account just for taxes

– One hour per week to:

– Categorize expenses

– Record income

– Move your tax percentage into the tax savings account

– One professional check-in per year (or at least in your first serious year)

If you prefer DIY but want structure, using one of the self-employed tax preparation services online can bridge the gap between full-service accounting and total solo chaos.

—

Checklist: Avoiding the Classic New-Freelancer Tax Traps

Use this quick list to pressure-test your setup:

– [ ] I set aside 25–30% of my freelance income for taxes

– [ ] I understand what self-employment tax is and that it’s in addition to income tax

– [ ] I know my next quarterly tax payment due date

– [ ] I use a separate account for business income and expenses

– [ ] I keep digital copies of receipts and invoices

– [ ] I track small recurring expenses (software, domains, tools)

– [ ] I’ve used either specialized software or consulted a tax professional at least once

If you can tick most of these off, you’re already ahead of a large chunk of new freelancers.

—

Final Thoughts: Treat Taxes as Part of the Job, Not an Afterthought

Freelancing gives you control over your work, but it also hands you the responsibility that employers used to handle quietly in the background.

Once you:

– Understand how self-employment tax works

– Get comfortable with quarterly payments

– Set up a simple system for tracking income and expenses

…tax season stops being a crisis and becomes just another admin task you know how to manage.

Start small: separate your accounts, choose a tool or service you trust, and make tax planning a regular part of your business—not a once-a-year panic.