Most people hear “50/30/20 budget” and think of a neat pie chart that magically solves money stress. In real life, though, your income is lumpy, rent is insane, and some months just blow up. The goal isn’t to squeeze your life into a rigid formula, but to bend the formula so it actually serves you. Let’s rebuild the 50/30/20 rule from the ground up, with room for messy schedules, side gigs, kids, and everything in between.

Where the 50/30/20 Rule Really Came From (and Why It Still Matters)

The 50/30/20 rule didn’t fall from the sky on TikTok. It became popular after Senator Elizabeth Warren and her daughter Amelia Warren Tyagi described a simple way to divide take-home pay: 50% for needs, 30% for wants, 20% for savings and debt. It was designed as a flexible framework, not a strict law. Back then, housing and healthcare were cheaper compared with income, and the typical earner had one main job and predictable paychecks. Today, with gig work, remote jobs spread across time zones, and rent that eats half a paycheck in many cities, a modern version has to be more forgiving. Think of it as a starting ratio you tweak, not a standard you fail.

Basic Principles: The Spirit, Not the Exact Percentages

At its core, the 50/30/20 method is about three buckets: survival, enjoyment, and future you. “Needs” are costs that trigger immediate consequences if you ignore them: housing, groceries, minimum loan payments, basic transport, essential medicine. “Wants” are everything that makes life feel like more than work-and-sleep: restaurants, streaming, trips, upgrades, hobbies. “Future” includes emergency funds, investments, and extra debt payments. If the classic split doesn’t work, keep the structure but move the sliders. Maybe it’s 60/20/20 in a high-rent city or 55/25/20 when you have big childcare bills. The principle is that every unit of your income has a job and no category silently expands without your permission. That clarity, not the exact ratio, is what calms your finances.

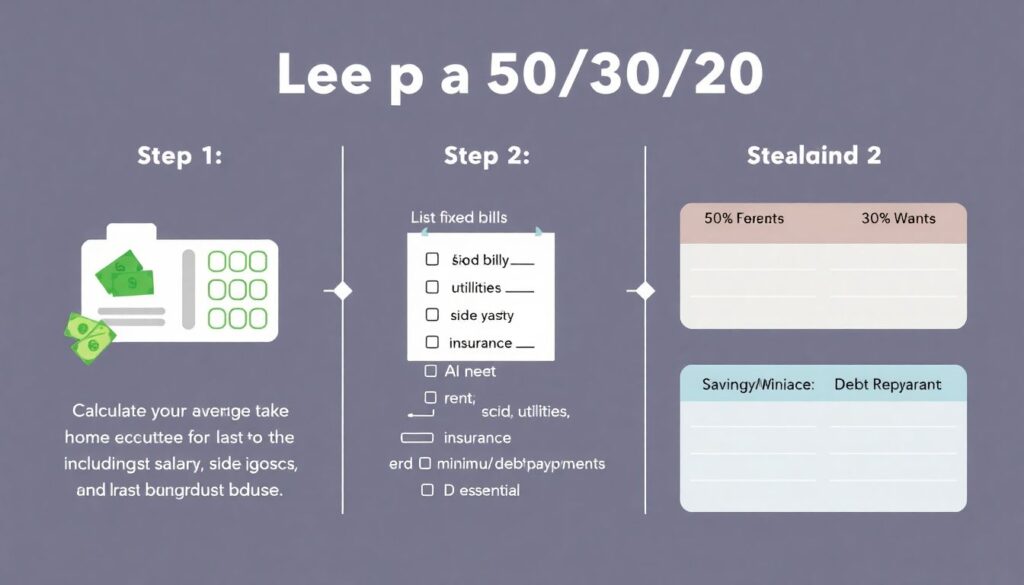

How to Set Up a 50/30/20 Budget Without Losing Your Mind

Understanding how to set up a 50 30 20 budget is easy in theory and annoying in practice, so simplify the process. First, calculate your average *take‑home* income over the last three to six months, including salary, side gigs, and irregular bonuses. Then list your fixed bills and label each as need or want, being brutally honest. Your gym may feel essential for your sanity, but financially it sits closer to “want” unless a doctor insists on it. Next, estimate variable spending like food and rideshares. Finally, decide what you can realistically send to savings and debt each month, even if it’s 5–10% to start. Don’t wait for the perfect number to begin. Start with a “draft budget” that hits any ratio and adjust over two or three months as you see where your real lifestyle pulls you off track. Treat this as an experiment, not a verdict on your self-discipline.

Non-Standard Twists to Make the Rule Fit Real Life

You’re not a spreadsheet, so your money plan shouldn’t pretend you are. One unconventional trick is to budget by *seasons* instead of strict months. If you know summer is travel-heavy or winter brings overtime pay, adjust your targets for those seasons. Another twist: use a “needs-plus” category for things that are not life-or-death but protect your income, like internet, childcare, or a decent laptop for remote work. You can let that category nibble into the 30% wants slice without guilt. For couples or roommates, create a joint 50/30/20 just for shared costs, then run separate, looser versions for your personal expenses. You can also flip the script and make your savings rate the fixed number, turning 20% into a “non‑negotiable bill” and forcing the needs and wants to share what’s left. This reverse engineering approach is uncomfortable for a month or two, but it’s powerful if you’ve struggled to save consistently.

Turning the Rule Into Action: Step-by-Step in Plain English

Instead of chasing perfection, you want a repeatable routine that runs mostly on autopilot. Try this sequence once, then refine it. First, plug your numbers into a simple 50 30 20 budget calculator online to see the “textbook” split; treat it as a reference, not a command. Second, open your banking app and tag the last 30 days of spending roughly as needs, wants, and future. Third, decide which two or three line items you’re willing to adjust right now—no more. Maybe it’s cooking one extra meal at home, canceling one subscription you barely use, or capping rideshares. Fourth, automate transfers to savings and debt payments the day after payday so the 20% bucket fills itself before the rest is touched. Finally, set a recurring ten-minute calendar reminder each week to glance at your balances and see if your real life is drifting from the plan. This weekly “money check-in” does more for your progress than any dramatic one-off overhaul.

Example: High-Rent City, Unpredictable Paycheck

Imagine you’re a freelancer in a big city, and rent is already close to 40% of your take‑home income. When you run the classic numbers, the 50% needs bucket is blown to pieces. Instead of giving up on the framework, you redesign it. You decide that in high-income months you’ll aim for 40% needs, 25% wants, and 35% future, knowing that leaner months might drop to 60/25/15. You build a “smoothing” savings stash that sits between your checking account and your long-term investments. In high months, the extra flows there; in low months, you withdraw to keep your needs under control. Your version of the 50/30/20 rule becomes a *range* instead of a single static number, which removes the guilt of not hitting the same target every month while still keeping your lifestyle from inflating beyond what your irregular income can safely sustain.

Example: Family With Kids and One Steady Salary

Now picture a household with one stable full-time earner and one partner doing part-time gigs while managing childcare. Between daycare, kids’ activities, and healthcare, the “needs” bucket feels endless. Here, a strict 20% savings rate might not fly yet. The solution is to zoom out to an annual perspective. Over twelve months, you map known spikes—back-to-school, holidays, birthdays, big utility bills—and pre‑plan mini-sinking funds for each. Maybe you settle on 55% needs, 25% wants, 20% future as the average for the year, but certain months dip or spike. You track progress quarterly instead of monthly, which smooths over temporary chaos like surprise dentist visits. Your 50/30/20 system turns into a rolling picture of your spending across seasons, letting you breathe during tough months without abandoning the entire strategy or raiding long-term savings every time life happens.

Quick List: Red Flags Your 50/30/20 Plan Is Too Rigid

– You feel like you’ve “failed” the moment a month doesn’t match the exact percentages.

– You refuse reasonable opportunities (like a networking trip or course) because they don’t fit neatly in wants or needs.

– You frequently move money out of savings to cover basic bills, which means your needs category is understated.

– You are tracking every cent but feel more stressed, not less, and avoid looking at your accounts.

Common Myths and Mental Traps About the 50/30/20 Rule

One big myth is that if you can’t hit 20% savings right now, the whole method is pointless. That belief keeps people stuck at zero progress. Even 3–5% saved consistently builds the habit and creates breathing room. Another trap is assuming every recurring bill is automatically a “need.” In reality, a surprising amount of fixed spending is negotiable: car choices, data plans, and convenience subscriptions creep into the necessities list without being questioned. There’s also the misunderstanding that the rule is only for salaried, middle‑class households. The logic—separating survival, comfort, and future—still helps if you’re on benefits, juggling student life, or managing several gigs. Finally, many assume they must track obsessively forever. In practice, the detailed tracking phase is temporary; once your categories stabilize, you can switch to lighter monitoring with occasional deep dives when your income or life situation changes.

Tools, Apps and Weirdly Helpful Workarounds

You don’t need fancy tools to manage this, but the right ones can make it painless. If you love your phone more than notebooks, try a 50 30 20 budgeting app that lets you create three main buckets and drag transactions into them. If you prefer something more analog but still structured, search for a 50 30 20 rule for budgeting template in your favorite note‑taking app and adapt it instead of starting from scratch. For spreadsheet fans, the best 50 30 20 budget spreadsheet is the one you actually open: skip ten-tab monsters and keep it to income, needs, wants, and future columns. And if your brain resists all of that, use physical envelopes or sub‑accounts at your bank. Name them “Must Pay,” “Fun Now,” and “Future Me,” and move money there on payday. The labels might feel silly, but they short‑circuit impulse spending more effectively than willpower alone.

Bullet-Point Playbook: Non-Obvious Tweaks That Actually Help

– Use “% bands” instead of exact targets. For example, aim for 45–55% needs, 20–30% wants, 15–25% future, and judge success by staying within the bands, not hitting one perfect number.

– Schedule “guilt-free splurge days” inside your wants budget so spending feels intentional, not like constant low-level cheating.

– Run a quick review after life events—new job, move, baby, breakup—and deliberately rewrite your 50/30/20 split instead of letting old numbers limp along.

– Once a year, treat yourself to a personal “money retreat”: one afternoon in a café to review the past year’s spending and rewrite your categories to match who you are now, not who you were when you started.

Bringing It All Together

A 50/30/20 budget that fits your real life is less about math and more about self-awareness. You’re not trying to impress a finance guru; you’re trying to avoid panic when bills hit and still enjoy your days. Start with the classic rule, run your numbers through a simple tool, maybe a 50 30 20 budget calculator, then loosen it until it matches your actual patterns. Expect the ratios to shift as your income, city, relationships, and priorities change. If you treat the rule as a flexible language for talking about money choices—rather than a judge of your worth—you’ll find it’s one of the few budgeting systems you can actually live with for years, not just a frantic month or two.

Комментарии