The invisible war in your head: “I need this” vs “I just want it”

You don’t overspend because you’re stupid or “bad with money”. You overspend because your brain is running 200,000‑year‑old survival software in a world full of one‑click purchases and 24/7 advertising. That clash is exactly why your budget keeps getting wrecked.

The tricky part? In the moment, your brain is absolutely convinced that a want is actually a need. That’s how you walk into a store for toothpaste and walk out with a new hoodie, snacks, and a candle that “was on sale so I’d be losing money *not* to buy it”.

Let’s unpack what’s going on in your head, then walk through a concrete, step‑by‑step method to stop your brain from sabotaging your money plans.

I’ll use real‑life style cases (based on typical client stories) so you can see how this plays out in practice—and how to handle it differently.

—

Why your brain keeps “needing” things you only want

Dopamine: the tiny salesperson in your brain

When you see something attractive—a new phone, shoes, upgrade, takeaway—your brain releases dopamine. Not when you *own* the thing, but when you *anticipate* getting it. Anticipation feels exciting, and your brain tags that excitement as important.

So in the moment, your brain says:

– “This will make me happier.”

– “I deserve this.”

– “I’ll figure the money out later.”

That’s not logic. That’s dopamine doing a persuasive sales pitch.

Short example from practice:

– Case: Sarah, the “I’ll just check the sale” shopper

Sarah wanted to save for a trip, but each month the money was gone. When we tracked her spending, most of it came from “quick looks” at her favorite clothing apps. She insisted: “But I *need* clothes for work.”

In reality, she already had more than enough outfits. Her brain had been trained: stress → scroll → see a sale → dopamine hit → “need”. Once she saw the pattern, she could change it.

—

Scarcity and FOMO: “If I don’t buy now, I’ll miss out”

Your ancestors survived by *not* missing chances: food, shelter, safety. Today, that same mechanism reacts to:

– “Only 2 left!”

– “Sale ends in 3 hours!”

– “Everyone’s going to that event!”

Your brain hears: “If I skip this, I’ll lose status, joy, or safety.”

So a want gets upgraded to a need in seconds.

– Case: Daniel, the “limited offer” spender

Daniel kept blowing his budget on “deal of the day” tech gadgets. Logically, he knew he didn’t *need* a third pair of headphones, but the timer on the site made him panic. Once we removed promo emails and used a 48‑hour rule for non‑essential purchases, the “urgency” vanished—and so did most of his random spending.

—

Emotion regulation: spending as self‑medication

Many people don’t overspend because they love stuff. They overspend because:

– They’re lonely, anxious, exhausted, or bored.

– Buying gives a quick feeling of control or comfort.

– They never learned other ways to soothe themselves.

In that moment, your brain isn’t asking, “Can I afford this?”

It’s asking, “Can this make me feel better *right now*?”

And almost anything that promises instant relief gets labeled as a need.

This is where financial therapy for money problems can help, because money patterns are often tangled with shame, childhood stories, and relationship conflicts—not just “bad math”.

—

Essential tools: what you actually need to outsmart your brain

You don’t need a 30‑tab spreadsheet and six bank accounts. You need a small set of tools you’ll actually use consistently.

Core tools

– A simple tracking system

Any method that answers: “Where did my money actually go?”

App, notebook, notes on your phone—it doesn’t matter, as long as you can see categories clearly.

– Budgeting apps for overspending

Apps like YNAB, EveryDollar, or simple bank‑linked tools can:

– Show you category limits in real time

– Warn you when you’re about to go over

– Make your “future self” visible: “If I buy this, my trip fund shrinks”

– A friction tool for spending

Examples:

– A 24–48‑hour waiting rule for non‑essential buys

– Purchases over $X require texting a friend or partner first

– Separate “fun money” account with a hard cap

Short and sweet: you want tools that slow down your decisions just enough for your rational brain to catch up with your emotional brain.

—

Optional but powerful tools

If you feel stuck or emotionally overwhelmed around money, consider:

– Guided support

Searching something like *personal finance coaching near me* can connect you with someone who helps you set up systems, practice scripts, and stay accountable—without judgment.

– Education with structure

An online money management course can give you step‑by‑step guidance if you like clear frameworks and homework.

These aren’t mandatory, but they greatly speed things up if you’ve been spinning your wheels for years.

—

Step‑by‑step process: retrain your brain to tell wants from needs

We’re going to walk through a practical, repeatable method. You don’t have to be perfect—just consistent enough that your new habits become automatic.

—

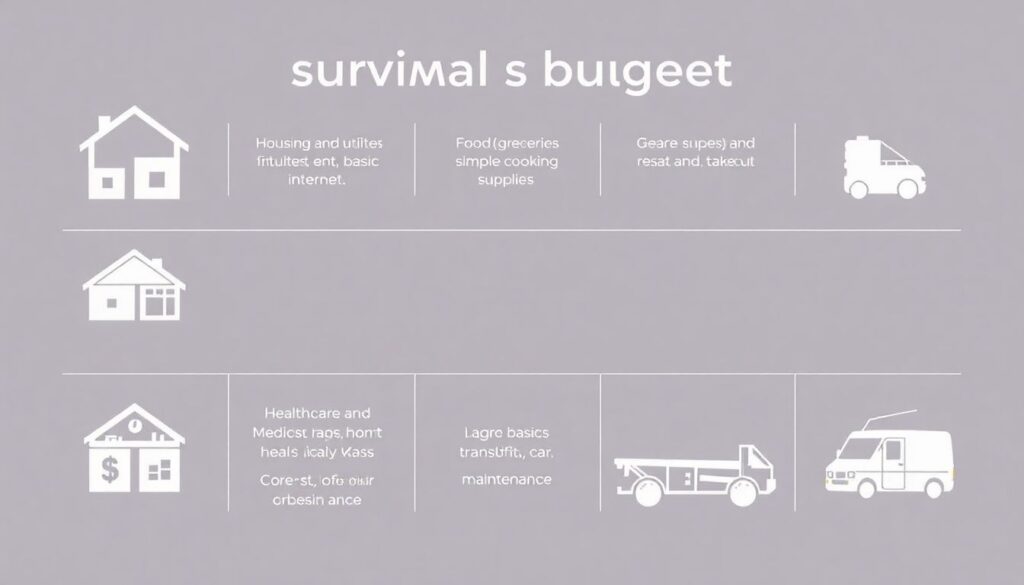

Step 1: Define *your* non‑negotiable needs

Before you look at any purchase, you need a stable definition of what “need” means in your life right now. If “need” is fuzzy, your brain will stretch it to cover everything.

Write down your current needs

Include only what keeps you safe, functioning, and able to work and live:

– Housing and utilities (rent, electricity, basic internet)

– Food (groceries, basic cooking supplies—not daily takeout)

– Healthcare and medication

– Basic transportation (gas, public transit, car maintenance)

– Core obligations (minimum debt payments, child expenses)

That’s it. This list will feel “too strict” at first. That’s normal. You’re not saying wants are forbidden; you’re just making the line *visible*.

—

Step 2: Create a “Wants with Boundaries” category

You’re not a monk. You’re a human who likes coffee, streaming, hobbies, and fun.

Instead of pretending you’ll never spend on wants, give them:

– A clear container in your budget

– A fixed amount per month

Example:

– Needs: rent, food, bills → funded first

– Goals: emergency fund, debt payoff, big savings → funded second

– Wants: restaurants, entertainment, clothes, treats → what’s left

Now you’re not asking, “Is this want allowed?”

You’re asking, “Is this want worth using part of my limited fun money?”

Over time, this question alone weakens impulse buying because you start comparing wants to each other, not wants to some vague idea of “I’ll save later”.

—

Step 3: Use a 60‑second pause before non‑essential purchases

This is the “mini‑interview” you run on every non‑need purchase.

You can do it mentally, but writing it down for a week or two is eye‑opening.

The 4 questions

Before you buy, ask:

1. Is this a need according to my written list, or is this a want?

(Force yourself to name it honestly.)

2. What emotion am I feeling right now?

Examples: bored, stressed, lonely, excited, proud, anxious.

3. If I don’t buy this today, what actually happens in my life?

Not imagined embarrassment or FOMO—concrete consequences.

4. In one week, will I remember this purchase or just the hit to my balance?

If you still want it after this, you’re free to buy—*as long as it fits inside your wants budget*. The goal is not zero wants; it’s conscious wants.

—

Step 4: Install “friction” where you’re weakest

Impulse spending usually clusters in 1–2 areas: food delivery, clothes, gadgets, subscriptions. You don’t have to fight everywhere at once. Attack your main leak.

Common friction tactics:

– Delete shopping apps that trigger impulsive orders

– Remove stored cards from your browser and phone

– Unsubscribe from promo emails and texts

– Set a “no-buy” rule for a specific category for 30 days

– Case: Maya, the late‑night delivery spender

Maya’s paycheck vanished into food delivery. We didn’t ban all delivery. Instead:

– She deleted the delivery apps.

– She planned two “delivery nights” per week, prepaid from her fun budget.

– She kept simple frozen meals for late nights.

Result: She cut food delivery by half without feeling punished, and finally built a starter emergency fund.

Friction works because it gives your rational brain time to come online. That’s exactly how to stop impulse buying and save money without relying on willpower alone.

—

Step 5: Run a weekly “Wants vs Needs” debrief

Once a week, spend 10–15 minutes reviewing where your money actually went. This is where your brain rewires.

Look at:

– Which purchases were true needs

– Which were wants you’re glad you bought

– Which were wants you regret or barely remember

Ask yourself:

– “What was I feeling before I bought this?”

– “What would I do differently next time?”

– “Did my budget match my real life this week?”

Over a month or two, you’ll start seeing patterns:

– “I overspend on Sundays when I’m lonely.”

– “Sales emails always get me.”

– “I underestimate restaurant costs.”

That awareness is the foundation of lasting change.

—

Real‑life patterns: three short case snapshots

1. The “I work hard, I deserve it” spiral

– Profile: 32‑year‑old engineer, good salary, no savings.

– Belief: “I need to treat myself or I’ll burn out.”

– Behavior: Weekly shopping, constant upgrades, expensive lunches.

Intervention:

– We didn’t ban treats. We changed the script to: “I deserve a secure future *and* joy.”

– He created a fixed “treat” budget and picked 2–3 high‑value joys (massages, one nice dinner) instead of daily random buys.

– We also added non‑spending rewards for stress: walks, gym, game nights.

Result: He kept feeling rewarded, but his monthly leftover cash went from $0 to $600.

—

2. The “Everything is an emergency” buyer

– Profile: Single mom, inconsistent income, high stress.

– Belief: “I can’t plan, something always comes up, so I have to grab things when I can.”

– Behavior: Overbuying kids’ clothes and supplies “just in case,” then short on rent.

Intervention:

– We built a tiny but real emergency buffer.

– We separated:

– Real emergencies (sickness, car breakdown)

– Predictable but irregular costs (school trips, clothing twice a year)

– She started labeling: “This is a future need, not a current need.”

Result: She stopped panic‑buying “just in case extras” and gradually built a more predictable spending rhythm.

—

3. The “I’m bad with money anyway” avoider

– Profile: Freelancer with debt, avoids checking accounts.

– Belief: “I always mess up; it’s hopeless.”

– Behavior: Emotional spending when feeling like a failure, then more shame.

Intervention:

– We started with financial therapy for money problems to unpack childhood messages (“Money is stressful”; “People like us are always broke.”).

– She practiced mini check‑ins with accounts, paired with neutral self‑talk: “This is just data. I’m allowed to learn.”

– We added one small, easy win: automatic $20/week to savings.

Result: Once money stopped feeling like a moral scorecard, her overspending dropped because she was no longer spending to numb shame.

—

Troubleshooting: when your brain wins and your budget loses

You *will* have slip‑ups. The goal isn’t perfection; it’s faster recovery and less damage each time.

Common problems and how to handle them

– Problem 1: “I keep justifying wants as ‘mental health needs’”

– Acknowledge that comfort and joy *do* matter.

– Still keep them in the “wants” bucket—just prioritize the ones that truly restore you.

– Ask: “Does this leave me feeling better 24 hours from now, or just for 10 minutes?”

– Problem 2: “I blow my whole fun budget in the first week”

– Split your fun money into weekly amounts, not monthly.

– Use cash or a separate account that you physically can’t overdraft.

– Add a rule: if you use next week’s fun money early, next week’s is smaller—no replenishing from savings.

– Problem 3: “I panic when I look at my spending, so I avoid it”

– Do 5‑minute reviews instead of full deep dives.

– Pair the review with something enjoyable: music, coffee, a comfy chair.

– Focus on curiosity, not blame: “What’s happening?” instead of “What’s wrong with me?”

—

When to ask for outside help

If you recognize any of these, outside guidance can speed up your progress:

– Money fights are constant in your relationship.

– You overspend when triggered by stress, trauma, or conflict.

– You’ve tried tools and apps for years but always end up back in the same cycle.

– Your debt or overdrafts are causing serious anxiety or sleep problems.

At that point, a blend of emotional and practical support helps most:

– A specialist offering something like *personal finance coaching near me* can help you build a custom system and practice new behaviors.

– A therapist familiar with money issues can help untangle deeper patterns.

– A structured online money management course can fill in knowledge gaps so you’re not guessing.

Reframing this as a skill you’re learning, not a character flaw you’re stuck with, is often the turning point.

—

Bringing it all together

Your brain isn’t trying to destroy your budget; it’s trying to protect you using ancient shortcuts: seek pleasure, avoid pain, don’t miss out. In a world designed to trigger those shortcuts, “wants” will always try to dress up as “needs”.

You don’t fix that with willpower alone. You fix it by:

– Clearly defining your real needs

– Giving wants a safe, limited space

– Adding friction where you’re weakest

– Doing quick weekly reviews to learn from your own patterns

– Getting help when emotions around money feel too big to handle alone

Run the 60‑second pause for a week. Notice what your brain says when it wants to upgrade a want into a “need”. That moment—right there—is where your financial future is decided, one small choice at a time.