Why Your Life Stage Should Drive Your Investment Plan

Most people start investing by asking, “What’s the best stock / fund / crypto right now?”

That’s the wrong question.

A better one: “What makes sense for *me* at *this* stage of life?”

That’s exactly what investment planning by age is about: matching your risk level, time horizon and cash-flow needs to the point you’re at right now, not to some generic “average investor”.

In other words, the core idea is simple:

> Your age and life stage don’t just influence your investments – they *constrain* and *enable* them.

Let’s walk through a step-by-step framework, compare a few common approaches, and see how to build a personalized investment portfolio by life stage without getting lost in jargon or hype.

—

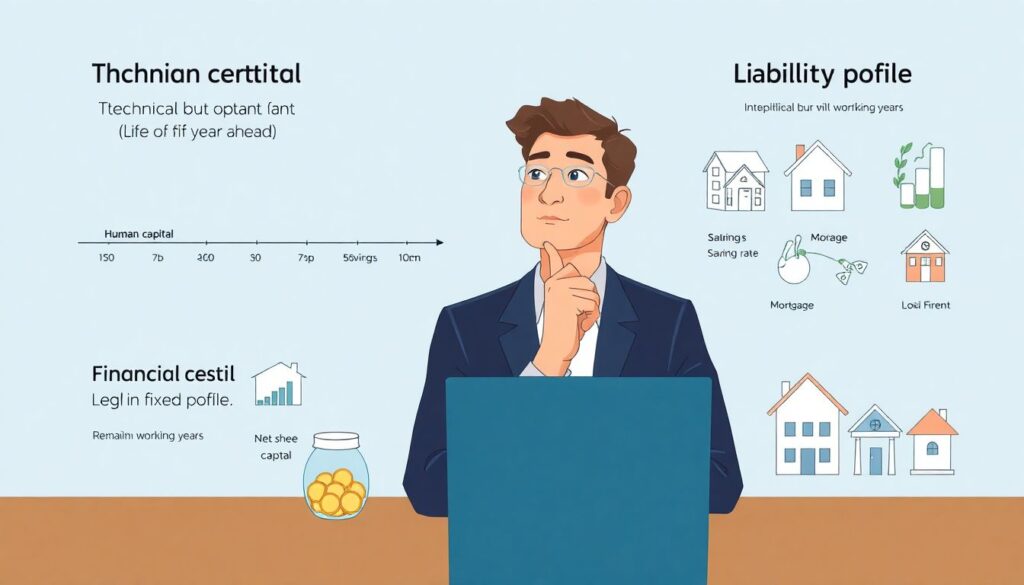

Step 1. Define Your Life Stage in Financial Terms

Forget labels like “young” or “close to retirement”. Think in balance sheet and cash-flow language.

Key financial factors by life stage

Ask yourself three technical but practical questions:

– Human capital: How many earning years do you realistically have ahead?

– Financial capital: What’s your current net worth and savings rate?

– Liability profile: How big and how rigid are your obligations (rent, mortgage, kids, loans)?

Your answers determine your risk capacity (what you *can* afford to risk) and your risk tolerance (what you can *emotionally* handle without panic-selling).

Two people at the same age can be in totally different situations:

– A 35‑year‑old doctor with rising income, no kids and low expenses

– A 35‑year‑old freelancer with unstable income and two dependents

Same age, completely different asset allocation logic.

—

Step 2. Pick Your Overall Strategy Type

Before getting into how to invest in your 20s 30s 40s 50s specifically, choose your general approach. Broadly, there are three main strategies, and you can combine them.

1. Age-based (glide path) strategy

You let your age and time horizon drive the mix of risky vs. conservative assets.

– More equities when you’re young

– Gradually more bonds / cash-like instruments as you age

This is the logic behind target-date funds and many default pension strategies.

Pros (why people like it):

– Very simple and systematic

– Automatically reduces market risk as retirement approaches

– Good for people who don’t want to babysit their portfolio

Cons (hidden downsides):

– Assumes your life looks “average”

– May be too conservative for high earners with late-peak careers

– May be too aggressive for someone with unstable income or health issues

—

2. Goal-based strategy

Instead of age, you focus on specific financial goals with their own timelines: house down payment, kids’ education, early retirement, etc.

You then build separate “buckets” of investments for each goal:

– Short-term goal (0–5 years): lower risk instruments, high liquidity

– Medium-term (5–15 years): balanced mix

– Long-term (15+ years): growth-focused

Pros:

– Highly aligned with your real-life needs

– Helps avoid mixing long-term money with short-term spending

– Makes market volatility easier to tolerate (you know which bucket is for what)

Cons:

– More complexity in tracking and rebalancing

– Requires discipline to keep money in the right bucket

– Can be over-engineered if goals constantly change

—

3. Income-based strategy

Here the focus is: “How much cash flow do I want or need from my investments?”

This is common in late-career and retirement planning: you emphasize dividends, bond coupons, rental income and structured pay-out strategies.

Pros:

– Very intuitive once you’re near or in retirement

– Directly linked to lifestyle sustainability

– Helps define what the best investment plan for retirement looks like *for you*

Cons:

– If started too early, can limit growth by overweighting yield over total return

– Income taxes may be higher depending on your jurisdiction

– Chasing high yield can push you into risky assets (dividend traps, junk bonds, etc.)

—

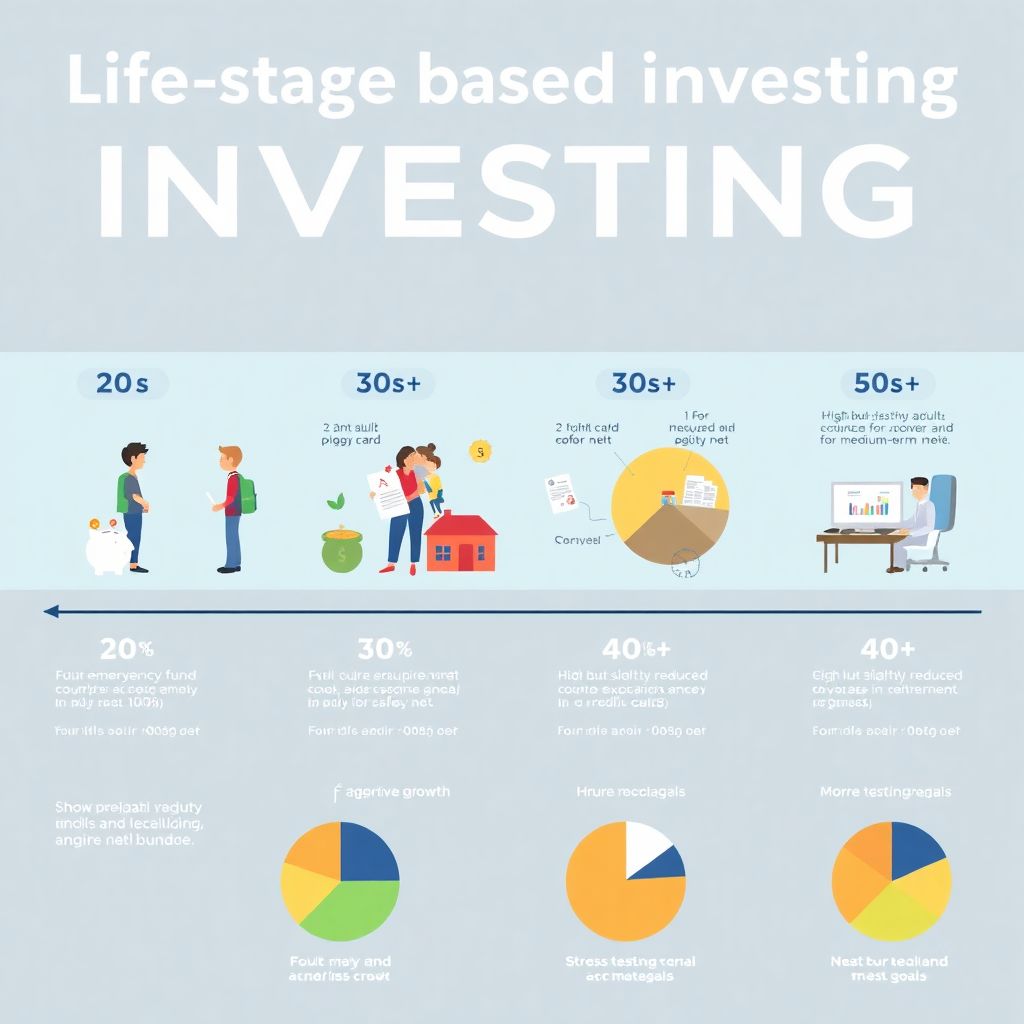

Step 3. Build by Decade: How to Invest in Your 20s, 30s, 40s, 50s

Now let’s apply these approaches by life stage and compare what changes.

In Your 20s: Aggressive Growth with Safety Nets

In your 20s, your human capital (future earnings) is usually far larger than your financial capital. That gives you a long time horizon and high risk capacity, even if your salary isn’t great yet.

Core priorities:

– Build a 3–6 month emergency fund

– Eliminate high-interest consumer debt

– Start investing in broad, low-cost equity funds (index ETFs or mutual funds)

From a technical standpoint, your equity allocation can often be 80–100% of your invested assets, *if* your safety net is in place.

Typical mistakes to avoid:

– All-in on speculative assets (individual stocks, crypto) before having a basic diversified core

– Ignoring retirement accounts and employer matches

– Stopping contributions after a market drop instead of using it as a buying opportunity

Here, a simple age-based or goal-based strategy usually beats over-optimized stock picking.

—

In Your 30s: Balancing Growth with Responsibilities

This decade often adds complexity: partner, kids, mortgage, career risks. Your income might rise, but so do fixed costs.

The main shift is from pure accumulation to risk management plus accumulation.

You still want high exposure to growth, but now:

– Insurance (health, life, disability) becomes a core risk management tool

– You might start creating separate “buckets” for kids’ education or a home upgrade

– Liquidity for career changes or entrepreneurship may matter more

This is where goal-based planning starts to shine versus a pure age-based glide path.

You might:

– Keep long-term retirement money in mostly equities

– Use a more balanced mix (say, 60/40) for medium-term goals

– Hold conservative instruments for near-term obligations

Working with a financial advisor for life stage planning can be especially useful here, because trade-offs multiply: pay off mortgage faster vs. invest more, fund kids’ college vs. your own retirement, and so on.

—

In Your 40s: Optimization and Risk Calibration

By your 40s, small decisions compound into large differences.

Here your focus becomes optimization:

– Fine-tuning asset allocation rather than inventing it from scratch

– Increasing tax efficiency (using tax-advantaged accounts strategically)

– Stress-testing your plan against bad market scenarios

You’re closer to key milestones, so sequence-of-returns risk (bad market returns near retirement) begins to matter. Many people start a measured shift towards a more balanced allocation:

– Still oriented to growth, but with a meaningful bond or defensive sleeve

– More detailed cash-flow planning for major expenses in the next 10–15 years

Compared to your 20s and 30s:

– You’re less able to “wait out” a lost decade in equities

– But you still need growth to avoid underfunding your future

This is where a hybrid strategy—age-based path adjusted by goal-based buckets—beats any one pure approach.

—

In Your 50s and Beyond: From Growth to Preservation and Payout

Once you’re in your 50s (and certainly in your 60s), the main transition is from “How big can I grow this?” to “How do I not run out of money?”

Two concepts dominate:

– Capital preservation: reduce the probability of permanent loss

– Sustainable withdrawal rates: align spending with portfolio capacity

Here, asking for the best investment plan for retirement is less about a universal recipe and more about:

– Your retirement age and desired lifestyle

– Your guaranteed income sources (pensions, annuities, rental income)

– Your health, dependents and inheritance goals

You’ll typically:

– Hold a higher share of bonds, cash and defensive assets

– Possibly tilt toward income-generating securities

– Maintain some equity exposure to prevent long-term purchasing power erosion

An income-based strategy now becomes a core layer, often sitting on top of a more conservative asset allocation.

—

Step 4. Comparing Three Practical Approaches

To tie it together, let’s compare how three real-world approaches treat the same life stages.

Approach A: One-size-fits-all “Aggressive Forever”

Some investors decide: “Equities outperform long term, so I’ll stay 100% in stocks forever.”

Strengths:

– Extremely simple implementation

– Maximum exposure to global growth

– Powerful compounding if you can tolerate volatility

Weaknesses (especially later in life):

– High vulnerability to a major crash right before or early in retirement

– Psychological strain; many people abandon this approach at the worst time

– No built-in mechanism to support stable withdrawals

This can work for highly risk-tolerant investors with flexible retirement dates and other income sources, but it’s usually too fragile as a universal model.

—

Approach B: Pure Age-based Glide Path (e.g., Target-date Funds)

Here, you choose a fund or rule like “110 minus age = % in stocks” and let it run.

Strengths:

– Automatic de-risking as you age

– No need to manually rebalance

– Good default for many workplace retirement plans

Weaknesses:

– Ignores individual differences in wealth, career path, and goals

– May push you too conservative if you’re behind on savings and have high risk capacity

– Or not conservative enough if you have health issues or unstable income

For many people, this is still a solid baseline. But it’s rarely optimal on its own when you have complex goals.

—

Approach C: Life-stage + Goals Hybrid (Recommended for Most)

This is where you combine:

– A high-level equity/bond mix guided by your age and risk capacity

– Multiple goal-based buckets with different horizons and risk levels

– A shift to partial income focus as you approach or enter retirement

Compared to A and B:

– It’s more work, but it lets you align every major decision—housing, kids, career change, retirement age—with your investment design

– It can be implemented gradually, starting simple and adding layers over time

– It matches how real life actually behaves: messy, not linear

This hybrid model is what many professionals mean by a personalized investment portfolio by life stage.

—

Step 5. When and How to Use Professional Help

You *can* DIY your investments. But as your life gets more complex—multiple goals, business ownership, cross-border issues—it can be rational to involve a specialist.

A financial advisor for life stage planning is useful when:

– You have several competing goals and limited capital

– You’re within 10–15 years of retirement and want to formalize a withdrawal strategy

– Large one-time events are coming: inheritance, business sale, relocation

However, not all advisors work the same way.

What to watch out for

– Pure product sales focus instead of holistic planning

– High, opaque fees that quietly erode returns

– Overly complex strategies that you don’t understand (complexity ≠ sophistication)

Look for:

– Transparent fee structure (flat fee or clear % of assets)

– Written financial plan with clear assumptions

– Willingness to explain trade-offs in plain language

—

Step 6. Operational Rules and Safety Checks

Once your life-stage strategy is chosen, you need simple operational rules to avoid emotional mistakes.

Basic rules for any stage

– Define a target asset allocation and a rebalancing rule (e.g., once a year or when any asset class drifts 5–10% from target)

– Separate “untouchable” long-term money from short-term cash needs

– Treat market crashes as a stress test, not a verdict on your intelligence

Common pitfalls that derail good plans

– Constantly changing strategy after reading new opinions

– Chasing recent winners (funds, sectors, or “hot” assets)

– Keeping too much idle cash out of fear, especially in early decades

To protect yourself, write down:

– Your investment policy (what you will and won’t do)

– Your decision triggers (when you’ll change allocation and why)

– Your deal-breakers (what would make you fire an advisor, exit a fund, etc.)

—

Step 7. Iterate Your Plan as Your Life Changes

Life stages aren’t fixed. Career shifts, health events, divorce, emigration, or entrepreneurship can all move you to a new financial reality overnight.

That’s why your plan needs a review cadence, for example:

– Quick check: annually (asset allocation, savings rate, contributions)

– Deep review: every 3–5 years or after major life events

In each review, reassess:

– Time horizon to key goals

– Risk capacity (income stability, obligations, buffers)

– Progress vs. plan: are you ahead, on track, or behind?

Then adjust:

– Contribution levels

– Asset allocation glide path

– Goal priority and timelines

This ongoing iteration is what truly makes your investments “fit your life stage”, rather than locking you into a model that no longer matches your reality.

—

Key Takeaways for Beginners

To wrap it up, here’s a compact checklist you can actually use.

– Start by mapping your life stage in financial terms, not just by age

– Choose a high-level strategy (age-based, goal-based, income-based, or a hybrid)

– Apply different risk levels to money for different time horizons

– Expect to adjust the plan as your life and markets evolve

And above all, remember: a “perfect” plan that you can’t stick to is worse than a “good enough” plan that you consistently execute. Aim for a robust, understandable structure that reflects where you are now—and leaves room for where you’re going next.