Why Big Life Moments Need a Structured Savings Plan

Major life moments — marriage, buying a home, having a child, retirement — have always existed, but the way we finance them has changed радикально. In the 1950s, a single steady job, defined-benefit pensions and cheaper housing often covered most goals by default. In 2025, volatile labor markets, longer lifespans and higher housing and education costs mean you need deliberate financial planning for major life milestones. Understanding how to save money for major life events is no longer a “nice to have” skill; it is basic financial infrastructure that protects you from high-cost debt and chronic money stress.

Step 1. Define Your Core Life Events and Time Horizons

Start by converting vague dreams into explicit “capital goals.” Make a list of events: wedding, home purchase, child-related costs, career change, and long-term retirement. For each, fix a time horizon: short term (0–3 years), medium term (3–10 years), long term (10+ years). This segmentation is the backbone of any savings strategy for life events like marriage buying a home and having a baby. Without clear time frames, you cannot choose appropriate risk levels, instruments or contribution amounts, and you end up underfunding everything equally.

Common Mistake: Mixing All Goals Into One Pile

A frequent error for beginners is maintaining a single generic savings account and mentally assigning it to every purpose at once. When a car breaks down or a vacation appears, the “future house” money evaporates. This behavioral trap, называемый mental accounting, leads to chronic goal slippage. Technically, you need separate “buckets” — distinct accounts or sub-accounts — for each large target. Even if they sit at the same bank, labeling and tracking balances independently helps you maintain discipline and avoid cannibalizing long-term goals for short-term impulses.

Step 2. Calculate Target Amounts Using Modern Benchmarks

Historical rules of thumb like “a year’s salary for a house” or “three months’ income for a wedding” no longer match 2025 realities. Instead, use current market data: local housing price-to-income ratios, average wedding costs in your region, projected childcare expenses and today’s retirement replacement-rate recommendations (often 60–80% of your final salary). Adjust for inflation expectations over your horizon. This approach transforms fuzzy hopes into quantified targets and aligns with best ways to budget and save for big life goals under modern economic conditions rather than mid‑20th‑century assumptions.

How to Divide Targets Across Monthly Contributions

Once you know target capital amounts and deadlines, compute required monthly contributions using a simple savings calculator or spreadsheet. Incorporate an assumed rate of return that matches the risk profile of each bucket: near 0% real return for cash, moderate for bonds, higher but volatile for equities. This transforms “I want a house someday” into “I must save $X per month for Y years.” If the math shows an impossible contribution level, that’s a signal to adjust: move the date, scale down the event, or add extra income streams rather than pretending the gap doesn’t exist.

Step 3. Build a Priority-Based Budget Framework

Now embed those contributions into your monthly cash flow. Instead of a generic 50/30/20 rule, use a hierarchy: essentials, mandatory savings, discretionary. Treat goal contributions as fixed obligations, not optional leftovers. Automation is critical: schedule transfers on payday to each goal bucket. The best ways to budget and save for big life goals in 2025 combine digital tools — banking apps, fintech budgeting platforms — with clear rules: pay yourself first, then live on the remainder. This mirrors how payroll pensions once worked, but now you’re the actuary managing your own mini‑pension fund.

1–2–3 Structure for Beginners

1. Establish an emergency fund covering 3–6 months of core expenses in a high‑yield savings account.

2. Contribute to retirement accounts up to any employer match — this is effectively a 100% return.

3. Allocate residual savings proportionally to mid-term goals (wedding, home, education).

For many novices, this 1–2–3 framework delivers a simple decision rule: no investing in speculative assets or luxury goals until the emergency buffer and basic retirement contributions are in place, reducing vulnerability to shocks.

Step 4. Decide How to Divide Savings Among Key Life Goals

A frequent question is how to divide savings for retirement wedding and house without shortchanging any of them. Use three criteria: time horizon, necessity, and flexibility. Retirement has the longest horizon but almost no flexibility — you cannot borrow from the future labor market indefinitely. Housing is partially flexible (location, size, timing) but heavily affects long-term stability. Weddings are most flexible in scale and style. Assign higher priority and larger percentage allocations to less flexible, higher-impact goals, and be willing to downshift optional aspects like wedding size if the math is tight.

Example Allocation Logic

Assume you can save 30% of take-home income after essentials. You might allocate 15% to retirement vehicles (401(k), IRA, workplace pension), 10% to a home down payment fund, and 5% to a wedding or other lifestyle events. When income rises, you proportionally increase these rates instead of inflating consumption. This dynamic allocation method ensures that as your career progresses, your capital formation keeps pace, echoing how post‑war households built wealth via rising contributions to savings plans rather than purely through wage growth or one‑time inheritances.

Step 5. Match Each Goal With an Appropriate Financial Instrument

Align each bucket with suitable asset classes and liquidity profiles. Short-term goals (0–3 years) like weddings or a planned baby fund typically belong in cash equivalents: high-yield savings, money market funds, short-term certificates of deposit. Medium-term goals (3–10 years) like a home purchase can incorporate a conservative portfolio of bonds with a modest equity component. Long-term retirement assets can justify higher equity exposure and tax-advantaged wrappers. This structured mapping is the technical heart of financial planning for major life milestones, preventing you from overexposing crucial near-term funds to market volatility.

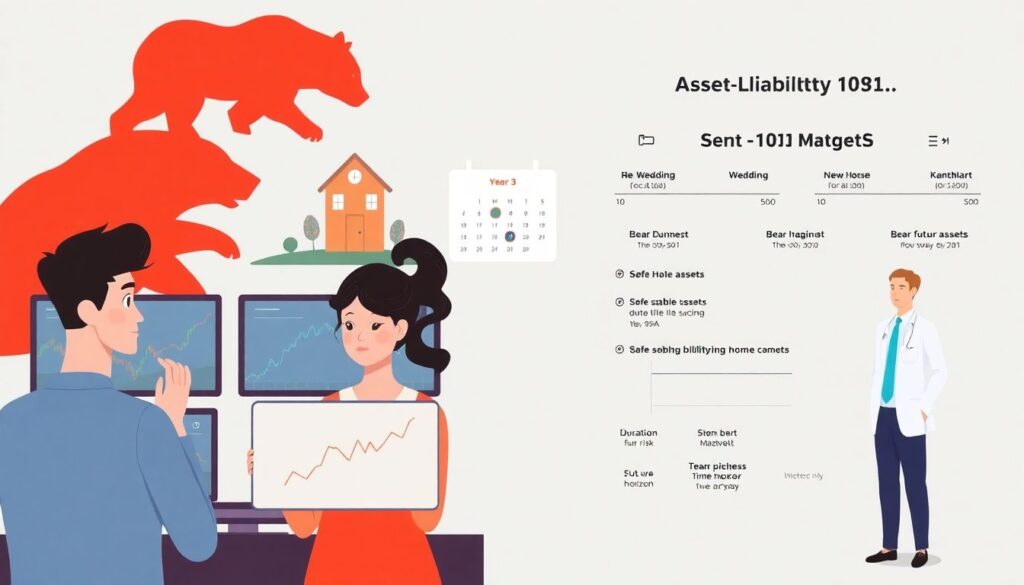

Risk Management Warning

New investors often chase yield on short-term money, putting wedding or house down payment funds into volatile stocks or crypto. If a bear market hits in year three, your timing is ruined. Professional practice uses asset–liability matching: assets whose risk and duration are calibrated to the liability (your future expense). As the event approaches, progressively de‑risk the associated portfolio — commonly called a “glide path.” This discipline echoes institutional pension management and is far more reliable than hoping markets bail you out just before you need the cash.

Step 6. Integrate Insurance and Contingencies

Historical financial systems relied heavily on extended families and state pensions to absorb shocks like illness or job loss. In 2025, more fragmented social structures and uncertain public benefits mean your savings plan must integrate risk transfer tools: health insurance, disability coverage, life insurance for dependents. Without this layer, a single medical event can destroy multiple goal buckets simultaneously. Consider term life insurance during years when you have dependents and significant obligations, ensuring your savings strategy for life events like marriage buying a home and having a baby is not derailed by low‑probability but high‑impact events.

Emergency Fund vs. Goal Funds

Keep your emergency reserve separated from goal-specific accounts, both practically and psychologically. The emergency fund stabilizes your household cash flow when income or essential expenses fluctuate, so you can maintain ongoing contributions even during stress. Raiding retirement or home savings every time there is a minor crisis is a structural design flaw, not bad luck. In technical terms, the emergency fund functions as a buffer stock of precautionary savings; only when it is full should you aggressively channel marginal dollars into higher-yielding but less liquid goal buckets.

Step 7. Monitor, Rebalance and Update for Life Changes

Life events rarely follow a clean timeline. Economic cycles, career shifts, and demographic trends (later marriages, later childbirth, remote work) should trigger periodic reviews of your structure. At least annually, reassess: goal timelines, contribution rates, asset allocation and risk tolerance. If your income increases meaningfully, redirect part of the raise into higher savings rates instead of letting lifestyle creep absorb everything. This iterative monitoring process is analogous to project management: you have a roadmap, but you must recalibrate as data changes, especially in a post‑pandemic, high‑rate, technologically shifting 2025 economy.

Behavioral Checkpoints

Schedule concrete checkpoints: set calendar reminders to review net worth, goal balances, and upcoming expenses. Track savings rates, not just account balances, since markets can distort temporary valuations. Use simple dashboards or apps to visualize each bucket’s progress relative to target. Many people abandon plans because they do not see incremental wins; visual evidence of trajectory counteracts that tendency. When targets are systematically ahead or behind, investigate causes: unrealistic assumptions, spending drift, or misaligned priorities. Adjust with intention, not out of frustration or panic during market noise.

Historical Context: From Informal to Structured Savings

Looking back 100 years highlights how unusual our current environment is. In the early 20th century, few households planned explicitly for college or long retirements; life expectancy was shorter, and extended families shared housing costs. Post‑WWII, rising real wages, government-backed mortgages and strong labor unions simplified long-term planning. By the 1980s–1990s, the shift from defined-benefit pensions to defined-contribution plans transferred risk to individuals, forcing them to self‑manage how to save money for major life events. By 2025, complex global markets and digital finance tools make structured, self-directed savings not only possible but essential.

What This Means for You in 2025

Today you have access to low-cost index funds, online retirement calculators and budgeting apps that past generations lacked, but you also face higher volatility in careers and asset prices. Instead of relying on a single employer or government program, you effectively run your own micro‑sovereign wealth fund across accounts and goals. The challenge is not information scarcity but decision overload. A clear, bucket-based structure turns this complexity into a systematic framework, helping you harness modern tools while mitigating modern risks associated with housing bubbles, student debt and pension uncertainty.

Practical Tips and Pitfalls for Beginners

Start small but consistent: even a modest automated transfer entrenches behavior and demonstrates feasibility. Avoid anchoring on social-media standards for weddings, homes or baby-related spending; calibrate your targets to your income, not to influencers. Use employer benefits aggressively, especially retirement matches and tax-advantaged accounts. Do not wait for “perfect conditions” to begin; inflation and lifestyle drift rarely wait for you. Over time, increase your total savings rate with each raise, keeping your lifestyle one step behind your income. This gradual escalation builds formidable capital without feeling like perpetual deprivation.

Frequent Errors to Avoid

Common pitfalls include underestimating irregular expenses (car repairs, medical copays), overestimating future self-control, and assuming career income will always trend upward. Another mistake is neglecting retirement while focusing solely on exciting near-term goals like a wedding or travel. Remember that compounding is time-sensitive; funds invested in your 20s and 30s exert disproportionate influence on later security. A robust structure intentionally allocates at least some fraction of every surplus dollar to long-term retirement, even when short-term milestones feel more emotionally salient.

Conclusion: Turn Life Moments Into a Deliberate Capital Plan

Major life events are predictable in category, if not always in exact timing. By explicitly defining goals, quantifying targets, prioritizing via a structured budget, aligning each bucket with appropriate instruments and regularly reviewing progress, you convert uncertain wishes into an engineered savings architecture. Instead of hoping the future “works out,” you act as your own planner, informed by historical context and modern tools. In a 2025 world where stability is less automatic, a disciplined, segmented savings structure is one of the most powerful forms of autonomy you can build.